[ad_1]

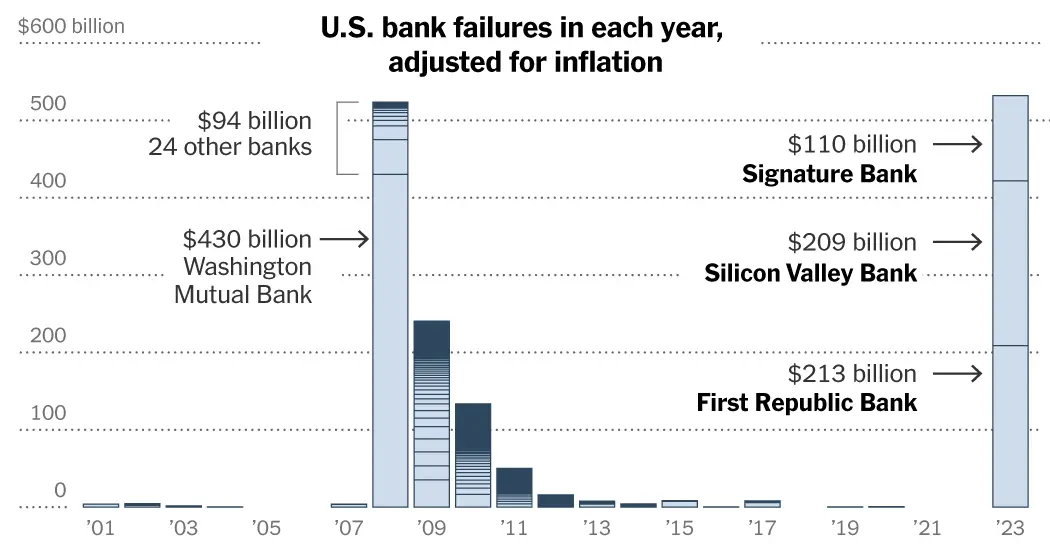

A bar chart of U.S. financial institution failures since 2001, displaying that First Republic Financial institution’s collapse was the second-biggest in U.S. historical past by way of belongings. The three banks that failed this 12 months have been price extra in inflation-adjusted belongings than the 25 that collapsed in 2008.

U.S. financial institution failures in every year, sized by whole belongings and adjusted for inflation

U.S. financial institution failures in every year, sized by whole belongings and

adjusted for inflation

Supply: Federal Deposit Insurance Corporation

Be aware: Information is as of Dec. 31, 2022. Chart contains failures of federally insured U.S. banks and doesn’t embrace funding banks.

By Karl Russell

Authorities regulators seized and sold off First Republic Financial institution on Monday, making it the third financial institution to fail this 12 months after Silicon Valley Financial institution and Signature Financial institution collapsed in March.

The three banks held a complete of $532 billion in belongings. That’s greater than the $526 billion, when adjusted for inflation, held by the 25 banks that collapsed in 2008 on the peak of the worldwide monetary disaster.

The implosion of Washington Mutual that 12 months, in addition to the funding banks Lehman Brothers and Bear Stearns, was adopted by failures all through the banking system. From 2008 to 2015, greater than 500 federally insured banks failed.

Most have been small or midsize regional banks and have been absorbed into different establishments, a typical end result for banks which were put beneath authorities management. Washington Mutual, which was closely concerned in dangerous mortgages and have become the most important financial institution to fail in U.S. historical past, was bought to JPMorgan Chase.

In recent times, fewer banks have gone beneath, thanks partially to stricter laws that have been put in place within the wake of the monetary disaster. Earlier than Silicon Valley Financial institution, the final financial institution to fail was in late 2020, because the coronavirus was ravaging the nation.

The collapse of Silicon Valley and Signature Financial institution in March led to fears of fallout for the broader business. Greater rates of interest have eroded the value of assets on banks’ stability sheets, stressing the monetary system and making it more durable for banks to pay again depositors in the event that they determined to withdraw their cash.

A bar chart itemizing the highest 30 U.S. banks by belongings on the finish of 2022. First Republic Financial institution ranks 14th, Silicon Valley Financial institution ranks sixteenth and Signature Financial institution ranks twenty ninth.

Largest U.S. banks by whole belongings

State Avenue Financial institution and Belief

Morgan Stanley Non-public Financial institution

Largest U.S.

banks by

whole belongings

State Avenue Financial institution and Belief

Morgan Stanley Non-public Financial institution

First Republic acquired a brief $30 billion infusion from the nation’s largest banks in March as a technique to restore purchasers’ confidence. However prospects pulled a staggering $102 billion in buyer deposits over the primary quarter of this 12 months, in line with the financial institution’s quarterly earnings report filed on Monday.

By the shut of buying and selling on Friday, the corporate’s stock price had dropped greater than 75 p.c this week.

Much like Silicon Valley Financial institution, First Republic had many start-up business purchasers, and plenty of of its accounts held greater than $250,000, the quantity lined by federal insurance coverage.

Prime 50 banks by share of deposits that aren’t federally insured

Excludes banking giants thought of systemically essential

A bar chart displaying the share of deposits that weren’t federally insured at 50 U.S. banks as of the top of final 12 months. At each Silicon Valley Financial institution and Signature Financial institution, greater than 90 p.c of deposits have been uninsured. At First Republic, this quantity was greater than 67 p.c.

Larger share of deposits uninsured

94% of $161 billion whole deposits

Bar heights are proportional to every financial institution’s whole home deposits

Larger share of deposits uninsured

94% of $161 billion whole deposits

Bar heights are proportional to every financial institution’s whole home deposits

Sources: Federal Monetary Establishments Examination Council; Monetary Stability Board

Notes: Information is as of Dec. 31, 2022. Contains home deposits solely. Excludes global systemically important banks, that are topic to extra stringent laws, together with more durable capital necessities.

By Ella Koeze

The laws put in place for the nation’s largest banks after the monetary disaster embrace stringent capital necessities, which suggests they will need to have a specific amount of reserves for moments of disaster, in addition to stipulations about how diversified their companies should be.

However midsize banks like First Republic, Silicon Valley and Signature wouldn’t have the identical regulatory oversight. In 2018, President Donald J. Trump signed a legislation that lessened scrutiny for a lot of regional banks. Silicon Valley Financial institution’s chief govt, Greg Becker, was a powerful supporter of the transfer. Amongst different issues, the legislation modified necessities for the amount of money that these banks needed to carry on their stability sheets to guard in opposition to shocks.

In a review of the Fed’s oversight of Silicon Valley Financial institution launched on Friday, Michael S. Barr, the central financial institution’s vice chair for supervision, stated the Fed would “re-evaluate” its guidelines for banks that have been related in measurement to Silicon Valley Financial institution.

Mr. Barr known as the financial institution’s failure a “textbook case of mismanagement.” However he faulted Fed supervisors, too, for not understanding the extent of the financial institution’s vulnerabilities, and for failing to take decisive motion once they did determine issues.

He additionally famous the true risk of contagion from Silicon Valley Financial institution. “A agency’s misery might have systemic penalties via contagion — the place issues about one agency unfold to different companies — even when the agency isn’t extraordinarily massive, extremely related to different monetary counterparties, or concerned in essential monetary providers,” he wrote.

[ad_2]

Source link