[ad_1]

The Russian struggle in opposition to Ukraine has each lowered gasoline provide to the EU and created dangers for future provide. The quantity of gasoline delivered from Russia to the EU fell to traditionally low ranges on the finish of 2022, reaching round 20% of pre-war ranges. The autumn in Russian gasoline exports to the EU began earlier than the struggle, leading to low gasoline storage ranges already at first of 2022. The response of the EU in implementing gasoline saving measures and sourcing different gasoline provides – significantly by tapping LNG markets – bolstered the buildup of gasoline in storage over the summer season of 2022. Such measures offered some reassurance in regards to the safety of gasoline provides for this winter, contingent on the climate not being too extreme. Nonetheless, the EU might face larger challenges when replenishing gasoline storage ranges forward of the 2023-24 winter. Particularly, as gasoline provides from Russia have dwindled, the EU has needed to flip to international LNG markets. Whereas this has alleviated quick provide issues, it has meant that gasoline provide and costs within the EU have change into extra delicate to swings in power demand from the remainder of the world, particularly from China. This field analyses the potential international dangers posed to EU gasoline provides in 2023 ensuing from shifts in Russian provide and Chinese language gasoline demand in a traditionally tight international gasoline market.

As provide from Russia has dwindled, the EU has turned to international LNG markets. Because of this, EU and Asian gasoline markets have change into more and more interlinked. Traditionally, gasoline costs in Asia have traded at a premium relative to the EU. It is because Asia relies upon extra on LNG to cowl fluctuations in gasoline demand, whereas the EU has had entry to cheaper pipeline gasoline, primarily from Russia (Chart A, panel a). This case modified after Russia curtailed pipeline provides to the EU and imposed unprecedented tightness on the EU gasoline market. To substitute Russian gasoline, LNG demand from the EU has risen over the past two years. Because of this, the correlation between EU and Asian gasoline costs has elevated considerably. It is because EU patrons are competing with Asian patrons and subsequently must pay a premium relative to Asian costs to draw the required LNG cargoes (Chart A, panel b). The correlation between EU gasoline costs and gasoline costs in america has elevated to a lesser extent, because the nation produces a lot of the pure gasoline that it consumes.

Chart A

Unfold between EU and Asian gasoline costs and gasoline worth correlations

a) Unfold between EU and Asian gasoline costs

(EUR/MWh)

b) Correlations of Asian and US costs with EU gasoline worth adjustments

(correlation coefficient)

Sources: Bloomberg and ECB workers calculations.

Notes: Panel a) exhibits the unfold between TTF and JKM month-ahead costs. Panel b) exhibits correlations between the TTF and JKM/Henry Hub every day adjustments in month-ahead costs.

A rebound in Chinese language LNG imports might constrain the EU’s capacity to safe gasoline provides all through 2023. Elevated EU gasoline imports in 2022 have been partly enabled by paying increased gasoline costs but in addition by a big drop in Chinese language LNG demand. China’s LNG demand in 2022 was 22 billion cubic metres (bcm) decrease than in 2021 (Chart B, panel a). Alongside decrease consumption in different nations and an growth in international LNG export capability, primarily in america, the EU was in a position to import considerably extra LNG than within the earlier yr (Chart B, panel b). The drop in Chinese language LNG imports in 2022 interrupted a decade of will increase in Chinese language gasoline demand. Partially, the droop in gasoline consumption could replicate China’s determination to modify to extra coal energy technology amid power safety considerations. Nonetheless, the primary driver was lowered gasoline consumption within the industrial sector[1], which was hit laborious by the lockdowns throughout 2022. On account of China’s exit from its zero-COVID coverage on the finish of 2022, elevated financial exercise will doubtless spur a rebound in LNG demand, including important strain to the worldwide LNG market, which is unlikely to see massive expansions in export capability till 2025.[2] This might constrain the EU’s capacity to draw LNG imports, particularly as a result of China has the proper to determine whether or not to purchase a pre-agreed quantity of LNG gasoline which quantities to a considerable share of world LNG cargoes.[3]

Chart B

Modifications in China’s gasoline demand and international LNG imports

a) Annual adjustments in Chinese language gasoline demand

(bcm)

b) Annual adjustments in international LNG imports

(bcm)

Sources: Bloomberg and ECB workers calculations.

Notice: In panel b, “Western Europe” contains Belgium, Finland, France, Gibraltar, Greece, Italy, Malta, Netherlands, Norway, Portugal, Spain, Sweden and the UK.

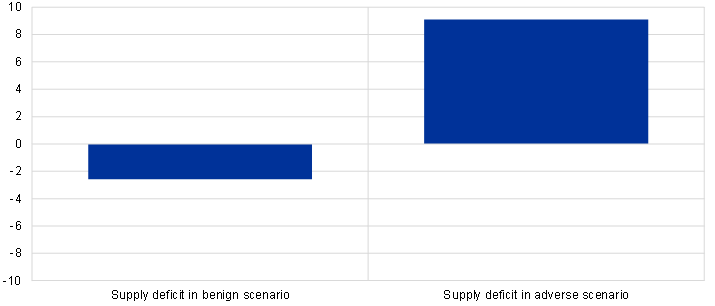

The dangers posed by a rebound in China’s power demand and a whole cut-off of Russian gasoline exports to the EU are highlighted by two illustrative eventualities for 2023. On the availability aspect, a benign situation assumes that flows of Russian gasoline to the EU proceed at present ranges. As a result of Russian gasoline deliveries have been lowered considerably all through 2022, Russia can be delivering on common about 40 bcm much less gasoline in 2023 than in 2022. It’s also assumed that a lot of the growth in international LNG capability in 2023 might be secured by the EU. An hostile situation assumes no Russian pipeline gasoline deliveries to the EU and a rebound in Chinese language power demand, which limits the EU’s capability to safe additional LNG imports. On the demand aspect, in each eventualities it’s assumed that the present EU-wide gasoline saving measures, at present solely in place till March 2023, are prolonged to the top of 2023. It’s also assumed that the EU will proceed to require gasoline inventories to be crammed to 90% capability forward of the winter.[4]

EU gasoline provide safety stays weak to international provide dangers and adjustments in demand (Chart C). Within the benign situation, the EU pure gasoline market can be broadly balanced, whereas within the hostile situation the gasoline deficit might account for about 9% of EU annual gasoline consumption. The deficit might fall to 4% if Chinese language LNG demand stays unchanged at 2022 ranges, or 2% if solely the dangers to Russian gasoline exports materialise. Such a deficit might in all probability be plugged by substituting gasoline with different power sources, rising power effectivity and implementing a average drawdown of inventories.[5] Nonetheless, EU gasoline safety in 2023 would stay weak to additional disruptions in gasoline provides or shifts in demand. Though the EU has considerably lowered its dependence on Russian gasoline, it has change into rather more delicate to swings in power demand from the remainder of the world, particularly from China.

Chart C

Two potential paths for the EU pure gasoline provide deficit

(percentages of projected 2023 consumption)

Sources: Eurostat, Refinitiv and ECB workers calculations.

Notice: Assumptions relating to gasoline consumption, manufacturing, exports and imports are based mostly on latest developments, the EU gasoline saving plan and the EU gasoline storage goal for the top of October 2023.

The problem for the EU to safe enough gasoline provides in 2023 can even rely upon the climate and depletion of gasoline inventories within the remaining a part of the 2022-23 winter. EU Member States have saved extra gasoline within the 2022-23 winter than envisaged by the EU gasoline saving plan, partly attributable to comparatively heat temperatures. Because of this, gasoline storage ranges have remained excessive and improved the outlook for gasoline provides in contrast with expectations earlier than the heating season began. Nonetheless, if temperatures drop severely or there’s a extended chilly spell within the coming months, gasoline inventories might deplete quicker than assumed in our evaluation, leaving EU gasoline markets in a extra weak place. On the similar time, heat temperatures throughout the winter months might place the EU in a stronger place to resist the challenges in 2023, whereas excessive temperatures in the summertime months would increase gasoline demand for electrical energy technology owing to an elevated want for air con.

[ad_2]

Source link