[ad_1]

Because the Price range 2023 proposed to cast off tax exemption from proceeds of insurance coverage insurance policies with very excessive worth, monetary advisors imagine that this might result in mis-selling, and due to this fact, traders are speculated to watch out earlier than shopping for a brand new coverage.

The brand new guidelines state that the place combination of premium for conventional life insurance coverage insurance policies (non-ULIPs) issued after April 1, 2023 is greater than ₹5 lakh; revenue from these insurance policies will probably be taxable.

Insurance coverage or tax saving instrument?

It’s crucial to notice that the insurance policies issued earlier than March 31, 2023 will probably be exempt from this new rule. This, imagine some consultants, is triggering mis-selling by insurance coverage brokers.

“The Price range 2023 has introduced that traders received’t get tax free advantages on maturity when the quantity of premium exceeds ₹5 lakh. So, now some brokers are urging the HNIs (excessive net-worth people) and extremely HNIs to purchase earlier than March 31 insurance coverage insurance policies which have premium of greater than ₹5 lakh in order that they’ll take advantage of tax profit earlier than the brand new modifications come into impact.

“However my suggestion is that one ought to take an insurance coverage coverage solely if you want it and never due to tax profit on the time of maturity. In spite of everything, it’s not a reduction supply that’s ongoing,” stated S. Sreedharan, a Sebi-registered funding advisor and co-founder of Wealth Ladder Direct.

Amol Joshi, Founding father of Plan Rupee Funding Companies, concurs and says: “Now we have all the time stated that in India in addition to globally, insurance coverage shouldn’t be handled as funding, however as a danger safety instrument. And if you lose tax profit past a sure threshold, it may be seen as yet another step in the direction of treating insurance coverage proper.”

Solely if you want it

It’s typically emphasised that coverage holders should purchase an insurance coverage coverage solely once they want it, and never as a result of it allows them to say a tax exemption, or another financial profit.

There are additionally speculations that the mis-selling will occur after the brand new rule come into impact subsequent fiscal. In spite of everything, there are a variety of exceptions to the rule and the proceeds is not going to be taxable in one of many three situations: when premium is decrease than ₹5 lakh, when coverage holder dies, or when the coverage is a ULIP.

However some say that the brand new guidelines are but not clear for insurers.

“The brand new rule will surely add to confusion as a substitute of mis-selling. Insurers are speculated to deduct the TDS. An insurer will deduct this tax solely when premium is above ₹5 lakh. Now for the reason that threshold is supposed to be computed on a cumulative foundation, one wouldn’t know whether or not the restrict has already been breached from the coverage holder’s facet, thus leaving the scope of tax open-ended. So, we are going to search for extra readability on this,” stated Tarun Chugh, MD & CEO, Bajaj Allianz Life Insurance coverage.

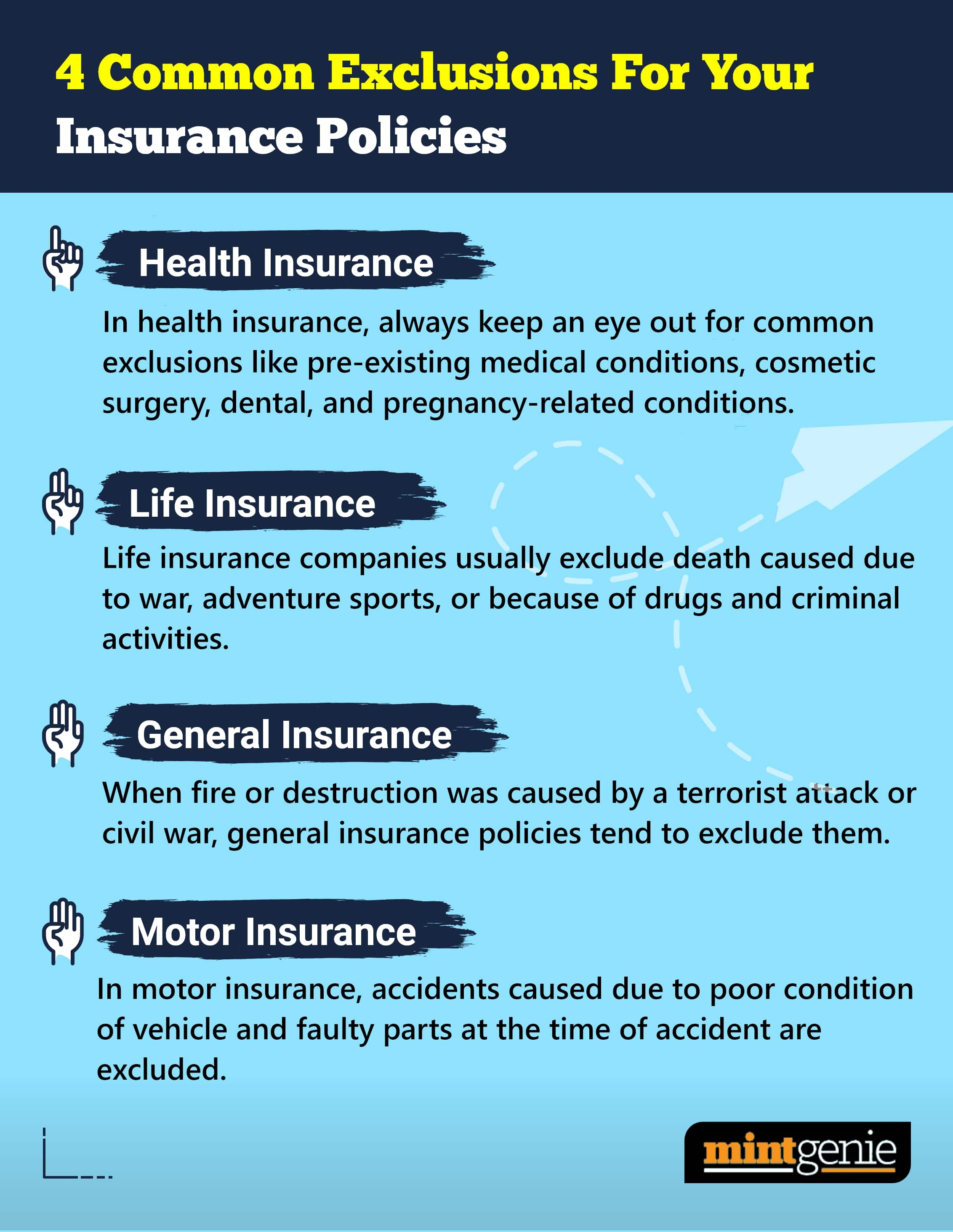

Widespread exclusions for insurance coverage insurance policies

First Revealed: 20 Feb 2023, 09:58 AM IST

[ad_2]

Source link