[ad_1]

On Might 3, 2023, the U.S. Securities and Alternate Fee (the “SEC”) adopted final rules requiring new disclosures associated to corporations’ share repurchase applications. The SEC claims the brand new guidelines will present buyers with enhanced data to evaluate the aim and impact of share repurchases. As mentioned in larger element beneath, the brand new and revised guidelines would require home corporations to, amongst different issues:

- Disclose every day repurchase exercise quarterly;

- Verify a field indicating if administrators or Part 16 officers traded within the related securities inside 4 enterprise days earlier than or after the general public announcement of an organization’s new or expanded repurchase plan or program;

- Present narrative disclosure in regards to the firm’s repurchase applications and practices in its periodic studies; and

- Present quarterly disclosure within the firm’s periodic studies on Kinds 10-Okay and 10-Q associated to its adoption and termination of 10b5-1 plans.

The ultimate guidelines require typically the identical substantive disclosures as initially proposed in December 2021, however the frequency and method of such disclosures have modified. For instance, the proposed guidelines would have required corporations to file a brand new kind (Type SR) disclosing the execution of share repurchases earlier than the top of the primary enterprise day following the repurchase. Within the last guidelines, nevertheless, the SEC dropped the Type SR requirement, opting as an alternative to require corporations to reveal every day quantitative repurchase knowledge on the finish of each quarter.

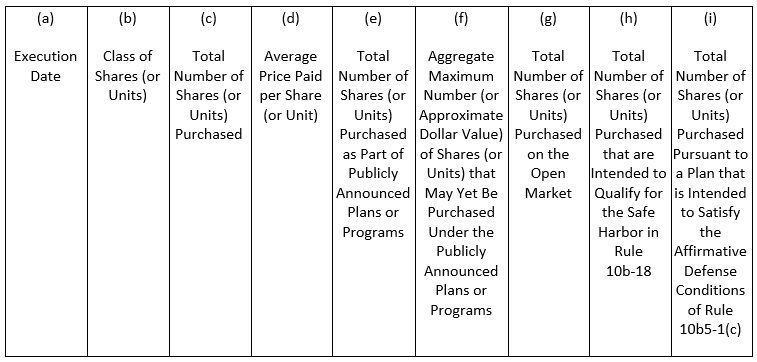

New Tabular Disclosure. The prevailing disclosure obligations in Merchandise 703 of Regulation S-Okay, which at the moment require aggregated month-to-month tabular disclosure of share repurchases in periodic studies, are being changed with new tabular disclosure reporting every day repurchase exercise that will likely be filed as an exhibit to both Type 10-Q or Type 10-Okay (for the fourth fiscal quarter). The brand new desk have to be formatted as laid out in Merchandise 601(b)(26) of Regulation S-Okay and XBRL tagged (the “New Repurchase Desk”). See Exhibit A beneath for a duplicate of the mandated New Repurchase Desk. As proven therein, corporations are required to reveal the next for every date on which purchases occurred through the relevant quarter:

- The category of shares bought;

- The whole variety of shares bought, together with, in a separate column to the desk, the overall variety of shares bought as a part of publicly introduced buyback plans or applications;

- The common worth paid per share, excluding brokerage commissions and different prices;

- The remaining buyback capability (in shares or {dollars}) remaining underneath any publicly introduced repurchase plan or program;

- The variety of shares bought within the open market;

- The variety of shares bought which might be meant to qualify for the Rule 10b-18 protected harbor;

- The variety of shares bought which might be which might be meant to fulfill the affirmative protection situations of Rule 10b5-1(c); and

- By footnote to the desk, the date any 10b5-1 plan was adopted or terminated.

The New Repurchase Desk have to be preceded by a checkbox requiring corporations to reveal whether or not any Part 16 officer or administrators bought or offered shares inside 4 enterprise days earlier than or after the announcement of (i) any new share repurchase plan or program or (ii) a rise in capability underneath any current plan or program. Firms ought to take into account whether or not to revise their insider buying and selling coverage to ban insiders from buying and selling inside 4 enterprise days previous to the bulletins concerning the corporate’s share repurchase plans or applications.

New Narrative Disclosure. To go with the New Repurchase Desk, Merchandise 703 of Regulation S-Okay has been revised and expanded to require corporations to offer the next narrative disclosure with respect to share repurchases:

- the goals or rationales for an organization’s share repurchases and the method or standards used to find out the quantity of repurchases; and

- any insurance policies and procedures referring to purchases and gross sales of the corporate’s securities by its officers and administrators throughout a repurchase program, together with any restrictions on such transactions.

In discussing goals and rationales for its share repurchases, corporations usually are not anticipated to disclose any aggressive or delicate data, although the SEC expects corporations to convey a radical understanding of the corporate’s goals or rationales for the repurchases and the method or standards it utilized in figuring out the quantity of the repurchases. The SEC additionally warned in opposition to utilizing boilerplate language, noting that the brand new narrative disclosure, along side the New Repurchase Desk, should present buyers with sufficiently detailed data to judge an organization’s share repurchases utilizing narrative appropriately tailor-made to an organization’s specific information and circumstances.

The SEC, counting on rule commentators, offered a non-exclusive checklist of instance disclosures that issuers ought to take into account discussing to keep away from boilerplate language, similar to discussing (i) different attainable methods to make use of the funds allotted for the repurchases, together with evaluating the repurchases with different funding alternatives that will ordinarily be thought-about by the corporate (similar to capital expenditures and different makes use of of capital), (ii) the anticipated affect of the repurchases on the worth of remaining shares, (iii) the components driving the repurchases, together with whether or not their inventory is undervalued, potential inner progress alternatives are economically viable, or the valuation for potential targets is enticing and (iv) the sources of funding for the repurchases, the place materials, similar to, for instance, within the case the place the supply of funding ends in tax benefits that will not in any other case be out there for repurchases.

Current disclosure necessities in Merchandise 703 will proceed (albeit in narrative slightly than tabular or footnote format), together with the obligations to reveal:

- The variety of shares bought apart from via a publicly introduced plan or program, and the character of the transaction (e.g., whether or not the purchases have been made in open-market transactions, tender affords, in satisfaction of the issuer’s obligations upon train of excellent put choices issued by the issuer, or different transactions); and

- Sure data with respect to any current repurchase plans or applications, together with (i) the date it was introduced, (ii) the greenback or share quantity licensed, (iii) the date of expiration (if any), (iv) whether or not any plan or program expired through the relevant quarter lined by the periodic report, and (v) whether or not the corporate has terminated previous to expiration, or not intends to make repurchases underneath, any plan or program.

New Merchandise 408(d) Disclosure concerning Rule 10b5-1 Plans. The SEC additionally adopted Merchandise 408(d) of Regulation S-Okay that may require corporations to reveal, together with in quarters by which no repurchases occurred, the fabric phrases (apart from pricing) of any 10b5-1 plan adopted or terminated by the corporate, together with the date on which the plan was adopted or terminated, the period of the plan and the mixture variety of shares to be bought or offered underneath the plan. If any disclosure required by Merchandise 408(d) overlaps with disclosures required underneath Merchandise 703 of Regulation S-Okay, corporations can cross-reference to such disclosure to fulfill Merchandise 408(d). This disclosure have to be XBRL tagged.

Compliance Dates. Home corporations are required to adjust to the brand new disclosure and tagging necessities of their periodic studies on Kinds 10-Q and 10-Okay (for the fourth fiscal quarter) starting with the primary submitting that covers the primary full fiscal quarter that begins on or after October 1, 2023 (for calendar yr corporations, this implies the Type 10-Okay for the yr ended December 31, 2023 filed in 2024).

Further Info. In case you have questions in regards to the guidelines mentioned above, please contact your Kutak Rock lawyer or one of many authors listed beneath.

SEC Adopts Final Rules Requiring New Disclosures Related to Companies’ Share Repurchase Programs

Exhibit A

Issuer Purchases of Fairness Securities

Use the checkbox to point if any officer or director reporting pursuant to Part 16(a) of the Alternate Act (15 U.S.C. 78p(a)), or for overseas personal issuers as outlined by Rule 3b-4(c) (§ 240.3b-4(c) of this chapter), any director or member of senior administration who can be recognized pursuant to Merchandise 1 of Type 20-F (§ 249.220f of this chapter), bought or offered shares or different models of the category of the issuer’s fairness securities which might be registered pursuant to part 12 of the Alternate Act and topic of a publicly introduced plan or program inside 4 (4) enterprise days earlier than or after the issuer’s announcement of such repurchase plan or program or the announcement of a rise of an current share repurchase plan or program.

[ad_2]

Source link

{kind=link}