[ad_1]

On this report, the Congressional Finances Workplace assesses its two-year and five-year financial forecasts and compares them with forecasts of the Administration and the Blue Chip consensus, a median of about 50 private-sector forecasts.

Variables Examined. CBO examines its forecasts of output development, the unemployment charge, inflation, rates of interest, and wages and salaries.

Measures of High quality. CBO focuses on 4 measures of forecast high quality—common error, common absolute error, root imply sq. error, and two-thirds unfold of errors—that assist the company determine the centeredness (that’s, the other of statistical bias), accuracy, and dispersion of its forecast errors.

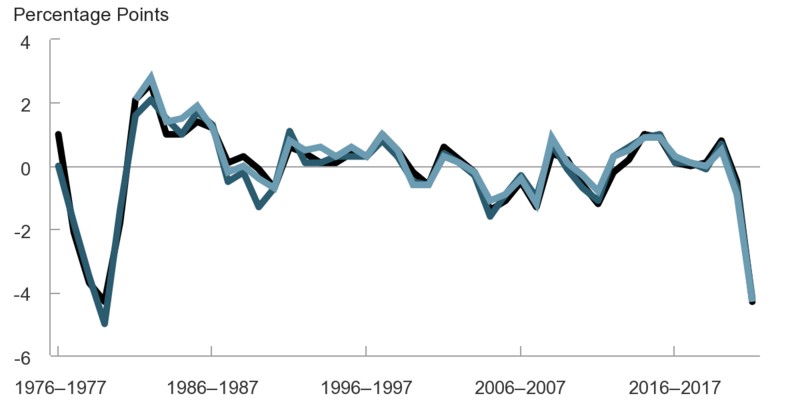

The High quality of CBO’s Forecasts. Most of CBO’s forecasts of output development, unemployment, and inflation have common errors near zero, however CBO’s estimates of rates of interest and wage development have been too excessive on common. As measured by the basis imply sq. error and the common absolute error, the two-year forecasts aren’t, on the entire, extra correct than the five-year ones.

Comparability With Different Forecasts. The diploma of centeredness varies by forecaster and variable. For instance, CBO and the Blue Chip consensus have a tendency to supply more-centered forecasts of output development however less-centered forecasts of rates of interest than the Administration does. CBO’s forecasts are usually extra correct than the Administration’s estimates and, for many variables, have the identical or smaller two-thirds spreads. For all 4 high quality measures, CBO’s forecasts are roughly corresponding to these of the Blue Chip consensus.

Sources of Forecast Errors. All forecasters didn’t anticipate sure key financial developments, leading to important forecast errors. The principle sources of these errors are turning factors within the enterprise cycle, modifications in labor productiveness developments and crude oil costs, the downward pattern in rates of interest, the decline in labor revenue as a share of gross home product, knowledge revisions, and the coronavirus pandemic.

Forecast Uncertainty. On this report, CBO makes use of previous forecast errors to gauge the uncertainty of its present forecasts. For instance, utilizing the basis imply sq. error, the company estimates that there’s an roughly two-thirds probability that financial development will common between 0.6 p.c and three.1 p.c over the following 5 years. CBO’s central estimate in February 2023 was 1.9 p.c.

[ad_2]

Source link