[ad_1]

Remarks by Philip R. Lane, Member of the Govt Board of the ECB, on the Panel Dialogue on Banking Solvency and Financial Coverage, NBER Summer time Institute 2023 Macro, Cash and Monetary Frictions Workshop

Cambridge, Massachusetts, 12 July 2023

Introduction

I’ll focus on this speech on the banking channel of financial coverage.[1] Beginning in December 2021 with the announcement that internet purchases beneath the pandemic emergency buy programme (PEPP) would finish in March 2022, the ECB has been tightening its financial coverage stance in response to the extraordinary surge in inflation amid the pandemic shutdowns, provide bottlenecks and, most significantly, the power disaster triggered by Russia’s unjustified battle in opposition to Ukraine.

For a given inflation outlook, the suitable degree and period of a restrictive financial coverage stance relies on how powerfully and the way shortly the financial system responds to the tightening of financial coverage. In view of the predominant function of the banking system in credit score provision within the euro space, how banks reply to financial coverage is a central difficulty in assessing the power of the transmission mechanism. Accordingly, in our data-dependent method to calibrating financial coverage, assessing the power of the banking channel of financial coverage tightening is a first-order activity for the ECB.

I’ll talk about among the challenges in forming a quantitative evaluation of financial coverage transmission through the banking channel.[2] First, I’ll briefly evaluate the assorted channels by way of which banks have an effect on the transmission course of. Second, I’ll assess how the appreciable quantity of financial coverage tightening injected over the past 12 months is being transmitted within the euro space.

The bank-based transmission of financial coverage

Financial coverage impacts funding and consumption choices by setting the extent of market rates of interest and thereby steering borrowing prices throughout all financial sectors: that is the “cost-of-capital” channel. When banks cross on modifications within the coverage charge to their debtors, the true financial system is affected through the funding and manufacturing plans of corporations, in addition to by way of the choices of households to financing consumption and actual property. Since for a lot of corporations and households the rates of interest that matter most are the lending charges and deposit charges set by banks, the pass-through of coverage charges to financial institution lending and deposit charges is a fundamental step in financial coverage transmission.

Along with the transmission through rates of interest, there are amplification mechanisms that work through the associated fee, the provision, and the standard of credit score and which can be in a position to generate comparatively giant actual results even with comparatively small financial coverage modifications. The primary amplification mechanisms working through banks are the steadiness sheet channel, the financial institution lending channel and the risk-taking channel.

The balance-sheet channel of financial coverage predicts {that a} coverage charge hike tends to compress asset costs and weaken exercise, thus reducing the online price of debtors.[3] This interprets right into a lowered capability to boost exterior funding for corporations: the rise within the exterior finance premium confronted by debtors attributable to a decline in internet price and pledged collateral decreases spending and funding by greater than what’s predicted by a short-term coverage charge change in a framework abstracting from the steadiness sheet channel. The identical channel additionally impacts households whose internet price is carefully linked to deal with costs. The decrease worth of collateral throughout a coverage tightening due to this fact triggers larger credit score danger and tighter credit score circumstances for each corporations and households.

The bank-lending channel focuses on the impression of coverage tightening on the provision of financial institution loans to the financial system. First, the provision of loans provided by banks is adversely affected by financial coverage tightening through a rise in financial institution funding prices.[4] Second, borrower-lender company prices additional scale back the willingness of banks to lend in periods of upper financial coverage charges or decrease financial exercise.[5] Third, financial institution steadiness sheet constraints amplify the contraction in credit score availability led to by coverage tightening.[6] Broadly talking, larger rates of interest enhance the chance price of holding probably the most liquid belongings – in a single day deposits – in contrast with much less liquid belongings similar to time period deposits or securities. Furthermore, the unwinding of asset purchases and long-term refinancing operations presently result in a direct decline within the liquidity out there to banks, limiting their capability to provide credit score.[7]

The third amplification mechanism is the risk-taking channel of financial coverage.[8] That is the channel by way of which banks are incentivised to make riskier investments in an setting of decrease rates of interest, which reduces incentives to interact in expensive monitoring.[9] As well as, asset purchases programmes extract period danger from the market, growing the relative attractiveness of riskier investments and due to this fact triggering a portfolio rebalancing that in the end results in a reallocation in direction of actual investments.[10] As such, in the course of the interval of extremely accommodative financial coverage, this may increasingly have led banks to construct up a inventory of dangerous investments. The alternative dynamic might not be working, as declining danger tolerance can result in a contraction within the provide of credit score.[11]

Every of the parts of the banking channel can work together with one another and generate self-reinforcing mechanisms that additional amplify the impression of the preliminary coverage impulse on credit score circumstances. As an example, following a financial coverage tightening, decreased financial institution danger tolerance coupled with weaker borrower internet price might have an effect on financial institution profitability and capital and due to this fact amplify provide constraints through the financial institution lending channel. Furthermore, basic equilibrium results additionally work together with the financial institution lending channel. Sturdy financial circumstances can present countervailing components that attenuate the impression of financial coverage, whereas weak macroeconomic circumstances might amplify the power of financial coverage tightening.[12] Specifically, as mixture demand falls in response to larger rates of interest, banks face each decrease demand for loans and a deterioration in borrower credit score danger which additional weigh on financial institution steadiness sheets. These extra components might additional strengthen the financial institution lending channel of financial coverage.

This temporary evaluate of the function of banks in financial coverage transmission has highlighted that the steadiness sheet channel, the financial institution lending channel, and the risk-taking channel could also be related within the transmission of the present climbing cycle. As well as, amongst different mechanisms, the rise in financial institution funding prices and the drop in liquidity might result in a contraction in credit score provide, adversely affecting bank-dependent corporations and households. Subsequent, I’ll evaluate the incoming proof on the power of financial coverage transmission through the banking system in the course of the present tightening cycle.

Measuring the banking channel of financial coverage tightening

I now flip to an evaluation of the incoming info on how the banking channel is working in the course of the present tightening cycle within the euro space. In June 2022, the ECB introduced that it might begin to enhance its coverage charges from July onwards. Nonetheless, it had already began unwinding its extremely accommodative financial coverage stance in December 2021, by asserting a step-by-step discount within the tempo of internet asset purchases, which pushed up yields of longer-dated belongings from early 2022 onwards.

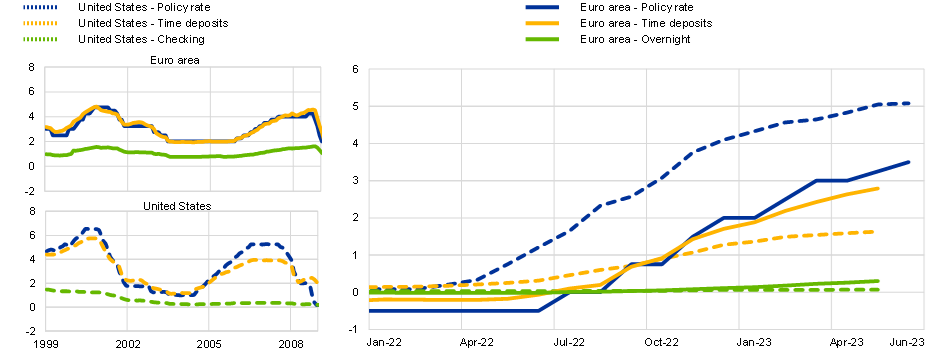

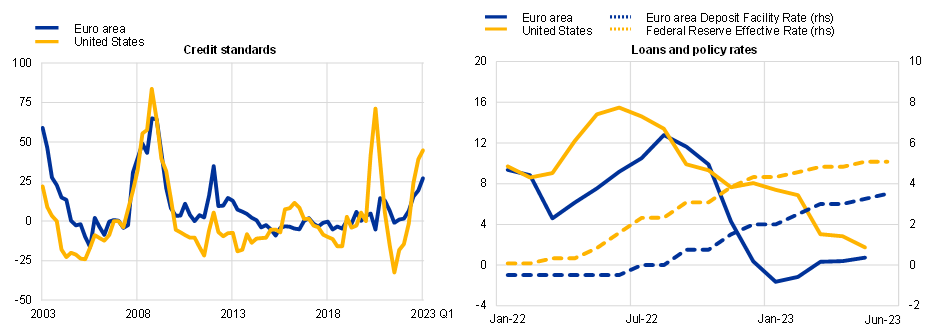

Towards the backdrop of the tightening of financial coverage, the pass-through to financial institution funding prices has proceeded quickly, most notably for yields on financial institution bonds (Chart 1).[13] Deposit charges contained the rise within the rate of interest bills of banks in the course of the preliminary section of the tightening cycle. This preliminary sluggishness was partly pushed by an atypical configuration of rates of interest in the course of the unfavorable charges interval, wherein many banks stored deposit charges larger than the coverage charge (Chart 2, proper panel). After this preliminary interval, rates of interest on time period deposits have adopted the coverage charge, whereas the remuneration of in a single day deposits has remained decrease. Total, these patterns had been additionally seen in previous intervals of optimistic rates of interest (Chart 2, left panel).

The restricted enhance in in a single day deposit charges has incentivised depositors to rebalance their portfolios in direction of time deposits, after the extended interval of low rates of interest and low time period premia wherein the chance price of holding in a single day deposit had been negligible. Evaluating developments within the euro space and the USA, whereas the pass-through to in a single day deposit charges is proscribed in each jurisdictions, the transmission to time deposits has been significantly stronger within the euro space (Chart 2).[14]

Chart 1

Euro space financial institution funding prices

(percentages)

Sources: ECB (BSI, MIR), IHS Markit iBoxx and ECB calculations.

Notes: Every day financial institution bond yields. Month-to-month deposit charges on new enterprise volumes weighted by excellent quantities. Composite funding price, calculated as a weighted common of the price of deposits and market debt funding, with the respective excellent quantities on financial institution steadiness sheets used as weights.

The newest observations are 4 July 2023 for bond yields and Might 2023 for BSI and MIR.

Chart 2

Deposit charge pass-through within the euro space and the USA

(percentages every year)

Sources: ECB (MIR, FM), RateWatch, FDIC and ECB calculations.

Notes: US coverage charge is the Federal Fund Price. Left panel: time deposits are the common charge on a 12-month CD with a minimal of USD10,000. Checking charges are the common charge on a USD 2,500 minimal checking account. Proper panel: time deposits are nationwide charges on 12-month CD for non-jumbo deposits (< USD 100,000). Checking charges are nationwide charges on non-jumbo deposits. The ECB coverage charge is the MRO as much as Might 2014 and the DFR thereafter.

The newest observations are June 2023 for coverage charges and Might 2023 for deposit charges.

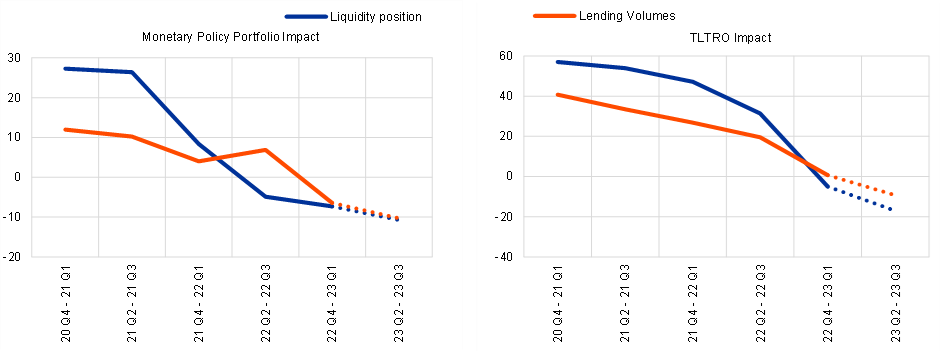

Along with the will increase in the important thing coverage rates of interest, the gradual unwinding of the asset buy programme (APP) and the phase-out of focused longer-term refinancing operations (TLTRO III) have additionally performed a task within the transmission of financial coverage by way of banks.[15] In February this 12 months, we moved to partial reinvestments beneath the APP earlier than absolutely ending reinvestments in July. The following decline in bonds held by the Eurosystem reduces the quantity of period extraction related to the excellent bond portfolio, and thereby will increase time period premia. The ensuing enhance in long-term rates of interest pushes up the pricing of financial institution loans, in the end growing lending charges for corporations and households. As well as, the upper yields on bonds enhance their attractiveness as an funding for banks, decreasing their incentives to provide loans.

Chart 3

Influence of the ECB’s financial coverage asset portfolio and TLTRO III on financial institution lending circumstances

(internet percentages)

Sources: ECB Financial institution Lending Survey (BLS).

Notes: Chart reveals the online proportion of banks reporting that modifications within the ECB’s financial coverage asset portfolio and TLTRO III had (a) a optimistic impression on lending volumes and (b) contributed to a rise of their liquidity over the related six-month interval. The ultimate interval denotes expectations.

The newest commentary for the BLS is the primary quarter of 2023.

The section out of TLTRO III has led banks to partially substitute TLTRO loans with costlier sources of funding. Whereas a big share of the voluntary early repayments on the finish of final 12 months and early this 12 months was financed out of excellent extra liquidity, banks have been extra lately elevating various funding to cowl maturing TLTRO loans, specifically in gentle of the big quantity which matured in June. The necessity to substitute TLTRO funding requires the issuance of extra expensive bonds and results in better competitors in deposit markets to draw funding. Moreover, the recalibration of TLTRO in October 2022 elevated the price of TLTRO borrowing, and restored incentives for voluntary early repayments. The ensuing enhance in financial institution funding prices put upward strain on lending charges and downward strain on credit score provide.

Furthermore, the winding down of each the TLTROs and the asset purchases has contributed to a fast discount within the central financial institution extra liquidity out there to banks. The mixed impact of this outright discount in liquidity provides downward strain on the provision of credit score by banks, as already evident in survey information (Chart 3). In distinction to the growth section, banks now report that the ECB financial coverage asset portfolio and the TLTRO III programme are related to decrease anticipated lending volumes, in addition to tighter anticipated credit score requirements and extra restrictive phrases and circumstances.

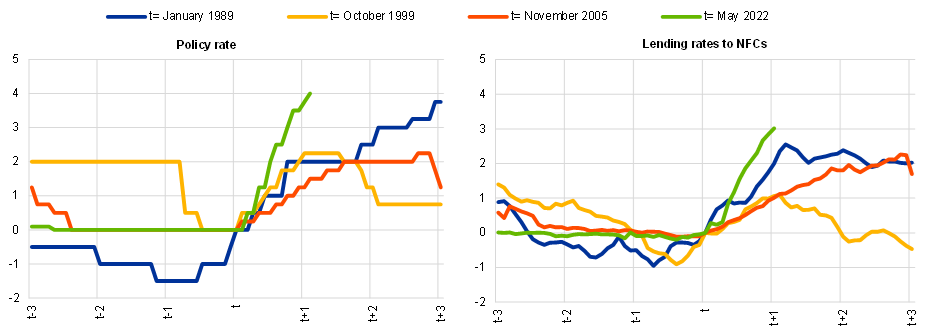

Turning to the lending charges for corporations, the pass-through of tighter financial coverage to total financing circumstances has been sturdy. Larger financial institution funding prices translated into a powerful enhance in lending charges to non-financial firms, though spreads relative to risk-free charges had been considerably compressed. Lending charges began to extend in June 2022 forward of the primary ECB charge hike. In contrast with previous climbing cycles, the present marketing campaign has seen probably the most distinguished lending charge enhance within the euro space – by way of each velocity and magnitude, additionally reflecting the unprecedented velocity and magnitude of coverage charge will increase (Chart 4).

On the similar time, mortgage volumes within the euro space have weakened sharply ranging from the top of 2022. Credit score flows have remained stagnant on mixture for loans and bonds, with some substitution between the 2 sources of financing (Chart 5, left panel). The weakening in credit score has been stronger than in previous climbing cycles and, whereas that is partly pushed by the unprecedented tempo of coverage tightening, a model-based simulation confirms that mortgage volumes circled sooner than what would have been anticipated primarily based on historic regularities, given the trail of financial coverage hikes since December 2021 (Chart 5, proper panel).

Chart 4

Lending charges to corporations throughout climbing cycles

(x-axis: years; y-axis: cumulative modifications in proportion factors)

Sources: ECB (MIR) and ECB calculations.

Notes: The ECB related coverage charge is the Lombard charge as much as December 1998, the MRO as much as Might 2014 and the DFR thereafter. t marks the beginning of every climbing cycle.

The newest observations are Might 2023 for lending charges and June 2023 for the coverage charge.

Chart 5

Agency debt financing flows and BVAR simulation of modifications in lending volumes

(left panel: common month-to-month flows in EUR billions; proper panel: x-axis: years, y-axis: progress charge of credit score in deviation from its progress charge firstly of the cycle (t), in proportion factors)

Sources: ECB (BSI, CSEC) and ECB calculations.

Notes: MFI loans are adjusted for gross sales and securitisation and money pooling. The seasonal adjustment of the online issuance of debt securities is just not official. Beginning months correspond to the month instantly previous the primary hike or express announcement of the hike of the cycle. The dotted line corresponds to a BVAR counterfactual for lending volumes, taking December 2021 because the final commentary and projecting volumes conditional on the trail of financial coverage charges. The kind of BVAR used is the one by Altavilla Giannone, and Lenza (2016).

The newest observations are for Might 2023.

The present tightening cycle has been broadly synchronised amongst main superior economies however the downturn in lending dynamics has been starker within the euro space than in the USA, regardless of the later begin of the climbing cycle and smaller magnitude of charge hikes to this point (Chart 6, proper panel). In each the euro space and the USA, the weakening of mortgage volumes was related to a powerful tightening of credit score requirements, as reported by banks within the euro space Financial institution Lending Survey (BLS), and within the US Senior Mortgage Officer Opinion Survey (SLOOS) (Chart 6, left panel). This proof factors to tighter mortgage provide in each economies. This tightening combines the reversal of beforehand extremely accommodative circumstances and the additional shift into extra restrictive territory in latest occasions.

Chart 6

Change in credit score requirements and company mortgage dynamics for United States and the euro space

(left panel: internet percentages, proper panel: left: three-month annualised progress charges, proper: percentages every year)

Sources: Haver analytics and ECB (BLS, BSI).

Notes: Credit score requirements for the USA correspond to the Senior Mortgage Officer Opinion Survey on financial institution lending practices, internet proportion of home respondents tightening requirements for Business and Industrial loans for big and medium banks. The precise panel reveals loans and leases of domestically chartered banks for the USA.

The newest observations are for the primary quarter of 2023 for credit score requirements, Might 2023 for loans and June 2023 for charges.

In fact, mortgage volumes and lending charges are the product of each credit score demand and credit score provide forces. Establishing the respective contributions is essential to grasp the underlying sources of credit score fluctuations, even when the underlying credit score demand and credit score provide schedules are unobservable. Whereas the proof from surveys and mixture information is beneficial in exhibiting wherein route credit score circumstances are travelling extra broadly, confounding components would possibly pose difficulties in decoding mixture measures. Certainly, taking a look at historic regularities, there’s a clear optimistic correlation between decrease bank-level mortgage demand and the tightening of credit score requirements. This is because of a number of components. As an example, corporations might ask for fewer loans when their expectations on the financial system deteriorate. This may occasionally result in an overestimation of the function of credit score provide if credit score demand is just not correctly estimated. On the similar time, banks might informally discourage their purchasers from making use of for loans and due to this fact not explicitly reject them. On this case, contemplating solely the a part of credit score provide that’s not associated to credit score demand can be a very conservative method that captures solely half of the particular change in credit score provide.

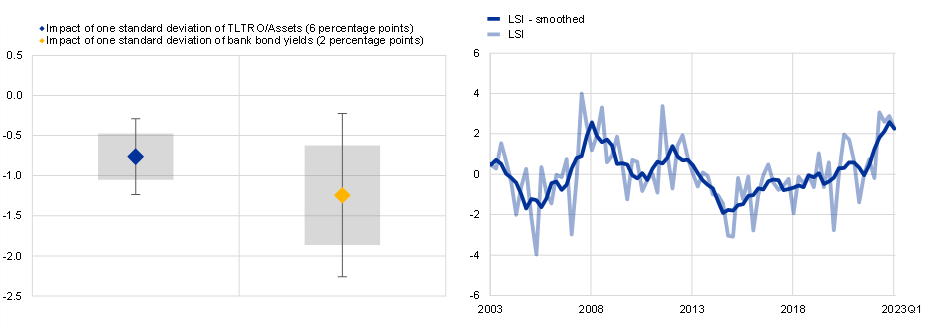

Elevated price of market-based financing and the phase-out of TLTROs has led to a contraction in financial institution credit score provide (Chart 7, left panel). Empirical evaluation that makes use of granular information to regulate for broader demand circumstances and thereby extracts a pure provide shock finds that each the discount in TLTRO funds and the rise in financial institution bond yields result in a major discount in mortgage provide. Particularly, the empirical estimates recommend that the decline in TLTRO for the reason that recalibration in October 2022 lowered quarterly mortgage progress by about 0.5 proportion factors, whereas the common enhance in financial institution bond yields for the reason that first charge hike in July 2022 led to a 1.1 proportion level decrease quarterly mortgage progress.

Chart 7

Drivers of mortgage provide restrictions and Mortgage Provide Indicator

(left: proportion factors, proper: index)

Sources: ECB (AnaCredit, iBSI, MOPDB), IHS Markit iBoxx, and ECB calculations.

Notes: Coefficients from a regression of three-months forward mortgage provide shocks (as in Amiti and Weinstein 2018), on TLTRO over belongings, and degree of financial institution bond yields, and financial institution fastened results and country-time fastened results. Pattern December 2019 to November 2022. Normal error clustered on the country-time degree. The precise panel reveals the Mortgage Provide Indicator (LSI) as in Altavilla, Darracq-Paries and Nicoletti (2019) and a smoothed model of it.[16]

The newest observations are November 2022 for the left chart and the primary quarter of 2023 for the LSI.

The function of credit score provide may also be remoted by utilizing smooth info from surveys. Particular person replies to the Financial institution Lending Survey can be utilized to assemble a Mortgage Provide Indicator (LSI) that purges credit score requirements from modifications in mortgage demand and prevailing macroeconomic circumstances (Chart 7, proper panel).[17] This indicator permits us to gauge how a lot of the noticed slowdown in credit score circumstances is because of provide results over and above the impression of financial coverage on credit score demand. The indicator reveals a marked contraction in mortgage provide for the reason that begin of the tightening cycle. This shift in mortgage provide circumstances is much more outstanding in view of the extremely accommodative mortgage provide setting within the years earlier than the pandemic.

Credit score provide restrictions sometimes result in a major drop in actual financial exercise. Augmenting a macro-financial empirical mannequin with the LSI signifies {that a} credit score provide shock resulting in a 1 proportion level decline in mortgage volumes leads to a 0.3 proportion level discount in actual GDP (Chart 8). A meta-analysis reveals that this quantification is according to the outcomes of different empirical research that use completely different fashions and canopy completely different pattern intervals and jurisdictions. Total, the outcomes point out {that a} credit score provide shock results in a contraction within the quantity of credit score intermediated by banks that in flip generates a considerable discount in output, in comparison with the baseline path.

Chart 8

The impression of credit score provide shocks on actual GDP

(proportion factors)

Sources: Gilchrist, S. and Zakrajšek, E. (2011); Barnett, W. A. and Thomas, R. L. (2014); Mumtaz, H., Pinter, G., and Theodoridis, Ok. (2018); Basset, C. et al. (2014); Altavilla, C., Darracq Paries, M., and Nicoletti, G. (2019); Chen, Ok., Higgins, P., and Zha, T. (2021); Gambetti, L. and Musso, A. (2017); Mendicino, C. et al. (2019); Jermann, U. and Quadrini, V. (2012); Gerali, A. et al. (2010); Darracq Paries, M., Kok Sorensen, C., and Rodriguez-Palenzuela, D. (2011); World Financial Outlook, IMF (2023); Barauskaitė, I. et al. (2022); Moccero, D. N., Darracq Paries, M., and Maurin, L. (2014); Ciccarelli, M., Maddaloni, A., and Peydro, J.-L. (2015). [18]

Notes: The chart reveals the distribution of the impression on actual GDP of a credit score provide shock throughout research. The vertical line represents the estimate obtained by utilizing the LSI as an exterior instrument in a Bayesian vector autoregressive (BVAR) mannequin to quantify the impression of a credit score provide shock on actual GDP progress. The stable blue line reveals the kernel density of the distribution of 15 estimates, truncated on the minimal and most estimate. The x-axis reveals the proportion ppomt decline in GDP cumulated over a three-year horizon of a credit score provide shock that reduces mortgage progress by 1 proportion level. The median impression throughout research is -0.3 proportion level and coincides with the outcomes of the LSI augmented BVAR.

Components affecting the power of the banking channel

Let me now talk about potential components that within the present setting can both attenuate or amplify the banking channel of financial coverage, beginning with three particular traits of this coverage cycle.

First, the present tightening consists of each everlasting and short-term parts. On the one hand, it concerned the unwinding of the terribly supportive financial coverage measures that had been in place since 2014 in an effort to fight persistent below-target inflation and mitigate the draw back dangers in the course of the pandemic. Within the absence of recent shocks that will drive the financial system again in direction of the decrease sure, the coverage charge is predicted to settle at round two per cent within the medium time period and extraordinary measures similar to large-scale quantitative easing and focused lending programmes are usually not anticipated to be re-introduced. It follows that this normalisation part is predicted to be primarily everlasting in nature. Alternatively, the hike of coverage charges into restrictive territory in the course of the first half of this 12 months displays a extra short-term part of the tightening cycle. Whereas the ECB will set coverage charges at sufficiently restrictive ranges for sufficiently lengthy to make sure a well timed return of inflation to our medium-term two per cent goal, the restrictive part of financial coverage will in the end be unwound in an effort to stabilise inflation at our goal somewhat than unleashing a subsequent section of chronically below-target inflation.[19] Earlier than the surge in inflation, it had been broadly anticipated that the “low for lengthy” coverage configuration would have endured for a number of extra years. Therefore, the everlasting part of the present tightening cycle would possibly amplify the banking channel in comparison with different tightening episodes which solely featured a purely cyclical tightening. Specifically, banks might extra extensively re-assess credit score provide insurance policies in response to the everlasting shift within the underlying financial coverage stance.

Second, the present setting of ample liquidity alters the mechanics of the financial tightening relative to earlier tightening cycles that came about inside coverage frameworks wherein the banking system operated with a structural liquidity deficit. Whereas the ECB steadiness sheet is shrinking, the de facto operational framework for financial coverage continues to be underpinned by ample liquidity whereby the deposit facility charge determines cash market circumstances.[20] The motion of the DFR into optimistic territory might induce a “chilly potato” impact, in that banks are incentivised to carry on to funds because the DFR is now optimistic, contrasting with the interval of unfavorable rates of interest.[21] On the similar time, the numerous decline in extra liquidity because of the contraction within the ECB steadiness sheet might result in better heterogeneity in cash market circumstances, particularly for the reason that distribution of the surplus liquidity is uneven throughout banks. In flip, because of this the responses to charge hikes are prone to be more and more heterogeneous throughout euro space banks and throughout member international locations, with related implications for the general impression of financial coverage tightening on the mixture euro space financial system.[22]

Third, the power of the banking channel of financial coverage plausibly differs throughout supply-driven and demand-driven inflationary episodes. The fading of a short lived demand shock is related to decrease incomes and output, amplifying the transmission of financial coverage by way of the banking channel. In distinction, the fading out of short-term provide shocks boosts incomes and provide capability. At present, that is the case for the reversal of the surge in power costs, the easing of provide chain bottlenecks, in addition to the post-pandemic re-normalisation of sectoral provide and demand circumstances. In a single route, the unwinding of a short lived provide shock places downward strain on inflation, decreasing the dimensions of financial tightening that’s required to return inflation to the medium-term goal in a well timed method.[23] Within the different route, the restoration in incomes attenuates among the transmission mechanisms through the banking sector, which must also be taken under consideration within the calibration of financial coverage.

We are able to flip to asking which components can have an effect on the effectiveness of our financial coverage, by way of these numerous channels. Normally, all else equal, there was a considerable discount in monetary tail dangers on account of the enhancements within the steadiness sheets of corporations and households that had been generated by pandemic-related fiscal transfers and the surplus financial savings accrued throughout pandemic shutdowns. The curtailment of tail dangers signifies that financial coverage is extra prone to transmit in an orderly method, somewhat than be disrupted by the emergence of systemic monetary stress. Certainly, the well being of the steadiness sheets of euro space corporations and households is mirrored within the only-limited deterioration in borrower defaults noticed to date on this tightening cycle.

For corporations, along with the mixture enchancment in steadiness sheets, comparatively excessive income over the past 12 months and elevated liquid holdings may act as attainable countervailing components. Nonetheless, there may be substantial variation throughout corporations. The information present that the corporations with larger revenue progress and better accrued money are typically these with comparatively decrease leverage. In different phrases, the aforementioned attainable mitigating components wouldn’t profit corporations that the majority want them: extremely leveraged corporations nonetheless stay uncovered to credit score tightening. Furthermore, the anticipated moderation of agency income over time may strengthen transmission.

As well as, granular information recommend that youthful and smaller corporations have been disproportionately affected by the decline in financial institution lending (Chart 9). Traditionally, such corporations have been the primary to undergo contractionary credit score provide shocks. The extra substantial contraction of lending dynamics for younger and small corporations will be interpreted as an indicator of a broader credit score provide tightening, the place banks begin defending their steadiness sheets in opposition to a deterioration of the cost capability of debtors. Given the danger of adversarial choice, banks decide to scale back credit score provide volumes somewhat than merely increase lending charges.[24] Moreover, the discovering that smaller corporations have seen a bigger tightening of credit score requirements is especially related in view of the central function that SMEs play within the transmission of financial coverage within the euro space, significantly by way of the financial institution lending channel. Such corporations, which account for a big share of employment within the euro space, are typically extra reliant on banks for lending and thus usually tend to expertise funding shocks when banks prohibit provide.[25]

Chart 9

Financial institution mortgage volumes of fringe corporations relative to the whole market for the reason that coverage hike

(ratios to total market developments)

Sources: ECB (CSEC, AnaCredit, RIAD), Orbis and ECB calculations. Notes: The chart compares mortgage charge and quantity dynamics of small and younger corporations relative to basic market actions across the begin of the climbing cycle in July 2022 primarily based on merged AnaCredit-Orbis information. The collection are standardised by total market developments in charges and volumes, and subsequently to unity firstly of the climbing cycle.

The newest commentary is for March 2023.

In assessing the impression of financial coverage tightening on each broader credit score dangers and the funding setting, the rising interconnections between non-bank monetary intermediaries and the euro space banking system require shut monitoring.[26] These hyperlinks account for 9 p.c of whole belongings and 14 per cent of whole liabilities of serious banks within the euro space on common. It follows that shocks to the non-bank monetary sector may enhance the credit score dangers and/or the funding prices of the euro space banking system. Specifically, since larger rates of interest broadly scale back the worth of belongings held by non-bank monetary intermediaries and enhance the funding prices of corporations which can be depending on market-based financing, these interconnections characterize an vital channel by way of which financial coverage tightening impacts the euro space banking system. Moreover, since non-banks have turn into more and more important credit score suppliers lately (particularly in some market segments), a contraction in credit score provide by non-banks needs to be included in an total evaluation of financial transmission, along with credit score provide intermediated by banks.[27]

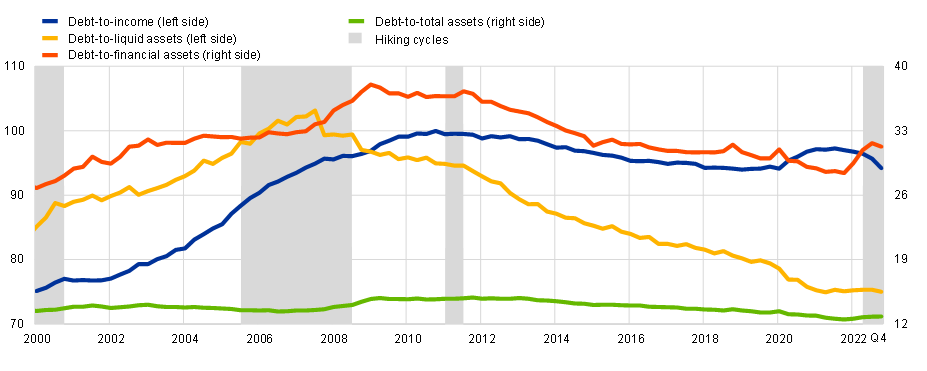

On the family facet, the altering composition of family steadiness sheets might have an effect on the power of the transmission of financial tightening through banks. In a single route, gross debt to revenue ratios, which measure debt servicing capability, at the moment are larger than within the 2000 and the 2005 tightening episodes, which might are likely to strengthen transmission (Chart 10). Within the different route, there’s a now a better share of fastened charge mortgages throughout the euro space, which may scale back the velocity of transmission by way of the cash-flow channel. Nonetheless, taking a look at how the present charge will increase have translated into larger charges on the inventory of mortgages, the distinction relative to the previous hikes doesn’t appear substantial. In different phrases, there is no such thing as a proof of a extra muted pass-through of upper charges to total mortgage lending.

In relation to the interconnection between housing markets and the banking channel, residential property makes up a excessive portion of family wealth. Information for the primary quarter of 2023 present a marked slowdown within the annual progress charge of nominal home costs for the mixture euro space and outright nominal worth declines in some international locations.[28] Reflecting this, the contribution of modifications in actual property asset holdings in direction of the expansion in family internet price has declined. The adversarial impression of declining asset values on family internet price suggests a extra highly effective steadiness sheet channel, with banks extra reluctant to supply mortgages or different credit score to home-owning households.

Wanting extra broadly at family steadiness sheets, households within the mixture now maintain a lot larger shares of liquid monetary belongings. Nonetheless, the true worth of cash holdings has been eroded by way of inflation, whereas capital losses have been incurred on bond holdings. Regardless of this, information for the primary quarter noticed a rebound within the annual progress charge of the online price of the family, partially pushed by enhancements in fairness costs in the course of the quarter. When it comes to distribution throughout households, liquid monetary belongings are largely owned by higher-income households, such that many households can’t draw down liquid monetary belongings to counter-balance any strain by way of debt channels.

Chart 10

Family steadiness sheet indicators

(percentages)

Sources: Eurostat, ECB (QSA) and ECB calculations.

The newest commentary is for the fourth quarter of 2022.

Shifting to the financial institution lending channel, financial institution capital and liquidity positions, in addition to the period of their asset portfolios, have an effect on the power of transmission. Ample capital and liquidity buffers, excessive profitability and acceptable credit score danger administration are vital to take care of the orderly transmission of financial coverage. Certainly, these components enabled the euro space banking system to face up to the market turmoil of March 2023 with out a extreme dislocation of credit score provide. Normally, in comparison with the previous, monetary stability dangers at the moment are extra carefully monitored by prudential authorities and are additionally topic to growing market scrutiny.[29] Subsequently, the precise realisation of economic stress is now much less seemingly in comparison with a counter-factual wherein banks had a lot decrease capital and liquidity positions.[30] On the similar time, since that is partly attributable to a extra cautious perspective of banks to rising dangers, it might contribute to a discount in credit score provide when confronted with a sustained weakening of borrower creditworthiness.

Equally, an extended period of the bond portfolios of banks may translate into larger unrealised losses from the autumn in bond costs, which can amplify the tightening of financial coverage.[31] As downward strain on financial institution income from these unrealised losses cumulates and mixture deposit volumes lower, banks turn into more and more uncovered to a tighter liquidity setting and must step up efforts to safe their deposit bases. Alongside this, whereas elevated competitors on deposit charges encourages transmission on one facet (in relation to dampening demand by households and corporations by making it extra engaging to carry deposits), there could also be an acceleration of the pass-through of the rate of interest hikes to deposit charges and broader funding circumstances to ranges incompatible with the goal deposit betas of banks. Such deposit betas underpin the asset and legal responsibility administration decisions of banks and dedication to traders, and thus a stronger pass-through might translate into elevated perceived banking sector danger and an extra discount in credit score provide.

The power of the risk-taking channel is underpinned by the upper danger perceptions across the macroeconomic outlook and the decrease danger tolerance of particular person banks. Growing issues concerning the credit score worthiness of particular person debtors might take a look at the flexibility of banks to fulfill capital targets, inducing a retrenchment from non-public sector credit score. In keeping with the BLS, danger perceptions proceed to be an vital driver of the tightening in credit score requirements. Partially, this may replicate a reversal of the impression of the risk-taking channel in the course of the accommodative phases of financial coverage, as danger tolerance declines and danger perceptions stay elevated. Decrease liquidity on the again of the contraction within the ECB steadiness sheet compounds this tightening strain by eradicating the leeway of banks to depend on excellent liquidity to fulfill current monetary obligations and shoulder idiosyncratic shocks. Even the online curiosity revenue of banks, which has expanded considerably for the reason that begin of the tightening cycle and has supported the general profitability of banks, levelled off within the first quarter of this 12 months, amid a stabilisation in intermediation margins and the stagnation in credit score volumes. Publicity to business actual property (CRE) may result in an amplification of financial coverage transmission, significantly if values fall in a sustained method. Growing funding prices put extra strain on this sector, which was already weak as a result of impression of adjusting working patterns on the demand for workplace area.[32] Furthermore, falling CRE asset values would result in a decline in borrower creditworthiness and collateral values, leaving banks uncovered to losses within the occasion of default. This might drive additional declines in lending provide, probably resulting in a monetary accelerator impact if such corporations are significantly financially constrained. It needs to be famous that regardless of elevated CRE dangers within the euro space, these are much less extreme than in the USA, with emptiness charges for euro space CRE decrease than these in the USA.

Let me conclude this half with two higher-level issues on the power of financial transmission through the banking system. First, given the worldwide nature of elevated inflation, the ECB is just not alone in growing coverage charges and there are spillovers from the worldwide charge hikes to euro space banks. Specifically, we must always see spillovers from hikes by the Federal Reserve and different international central banks to the funding prices and liquidity of worldwide energetic euro space banks, probably additional amplifying the financial institution lending channel by way of international tightening.[33] Second, whereas the resilience of the euro space financial system might have restricted the severity of the credit score provide channel by boosting the incomes of corporations and households, a downturn or reversal of those components would amplify the present slowdown in credit score. Specifically, because the cumulative tightening in financial coverage good points additional traction, the countervailing impression of those components will plausibly decline, with fading income or a slowdown in family incomes amplifying the impression of the credit score channel.

Conclusions

The banking channel is prone to additional strengthen within the coming months. The everyday lags in financial transmission imply that the complete financial impression of the appreciable financial tightening over the past 12 months will solely play out over the subsequent couple of years. In relation to the banking channel, transmission will proceed to strengthen with the continued repricing of financial institution funding, whereas the repricing of maturing fixed-rate loans will place additional upward strain on mixture lending charges. The decline in liquidity as a result of additional reimbursement of TLTRO funds and the shrinking of the APP portfolio will additional strengthen transmission through the banking channel within the coming months. Moreover, any deterioration within the macroeconomic setting would additionally reinforce the banking channel by decreasing mortgage demand and growing credit score dangers. Non-linear amplification results may materialise within the occasion that monetary stress emerges both within the euro space or overseas.

Wanting forward, we are going to proceed to observe the power of the banking channel by way of a spread of indicators that draw on each laborious and smooth info. As a part of our broad evaluation of the banking channel, we look at a big selection of indicators on lending circumstances, by way of info on financial institution steadiness sheets, the evolution of lending and deposit charges and survey-based measures. Our evaluation is pushed each by incoming information, but in addition broader modelling of financial institution lending circumstances to create a forward-looking evaluation. We mix macro-level information analyzing mixture euro space credit score developments and micro-level information that enables for variation throughout banks and completely different sectors of lending. The BLS performs a key function in our evaluation, because it permits us to separate the demand and provide parts of credit score developments. The April BLS indicated that the online proportion of banks that additional tightened their credit score requirements on loans to corporations within the first quarter was 27 per cent, whereas the online proportion of banks reporting a decline in demand was 38 per cent. These outcomes spotlight the function that each credit score demand and credit score provide are enjoying in the course of the present tightening cycle. The approaching July BLS will present recent info on the latest evolution of credit score demand and credit score provide, whereas the banks will even report their expectations for credit score demand and credit score provide for the approaching months. Accordingly, together with the broader banking, monetary and financial incoming information, the July BLS will assist us to replace our evaluation of the banking channel of financial coverage tightening.

[ad_2]

Source link