[ad_1]

By Kylie Purcell

A number of years in the past, robo-advisors had been the discuss of the funding business. Billed as the reply to expensive monetary recommendation, robo-advice platforms use standardized threat evaluation instruments to pair you with an funding portfolio — sometimes composed of ETFs.

By eradicating the human advisor element, they promised to revolutionize the business by making long-term investing and monetary planning cheaper and extra accessible to the plenty.

Now, there are indicators the robo-advice business could be dropping steam — at the least in its present kind.

Round 35% of adults within the U.S. have used a robo-advisor, in keeping with new survey information from Finder.com. However of these, barely greater than half have chosen to opt-out — 17% who actively use a robo-advisor v.s. 18% who now not do.

The explanations are unclear, however some consultants consider the dearth of human engagement is an even bigger barrier than many had perceived.

Shedding Steam?

Final 12 months, the sale of BlackRock’s robo-advisor platform FutureAdvisor to Ritholtz Wealth Administration despatched ripples by the business.

Hailed as a promising enterprise in 2015, the sale of FutureAdvisor by one of many world’s largest asset managers brings to query the position and profitability of the sector.

The expansion numbers appear to help this image.

Robo-advisor funds underneath administration are projected to achieve $2.76 trillion globally by the tip of 2023. However development has been on a largely downward development for half a decade — and is predicted to sluggish considerably within the subsequent few years, in keeping with a brand new report by Statista.

In 2021, property underneath administration grew by over 65% — in 2023, development is predicted to fall to 12.5% and simply 8% by 2027.

Australia, which has round half a dozen robo-advisors at present, has seen at the least 5 robo-advisors shut doorways in as a few years

And in July this 12 months, one of many nation’s earliest and hottest robo-advisors, Six Park, introduced it was winding down after simply 8 years in enterprise attributable to tough market circumstances.

Nonetheless a Want

Patrick Garrett, cofounder and CEO of the not too long ago defunct Six Park, believes unclear regulation round recommendation companies, somewhat than altering client demand, has hindered the expansion of robo-advice.

“There stays an unlimited unmet want for the mass market that can’t afford full-scale monetary recommendation to have the ability to entry an inexpensive funding administration service.”

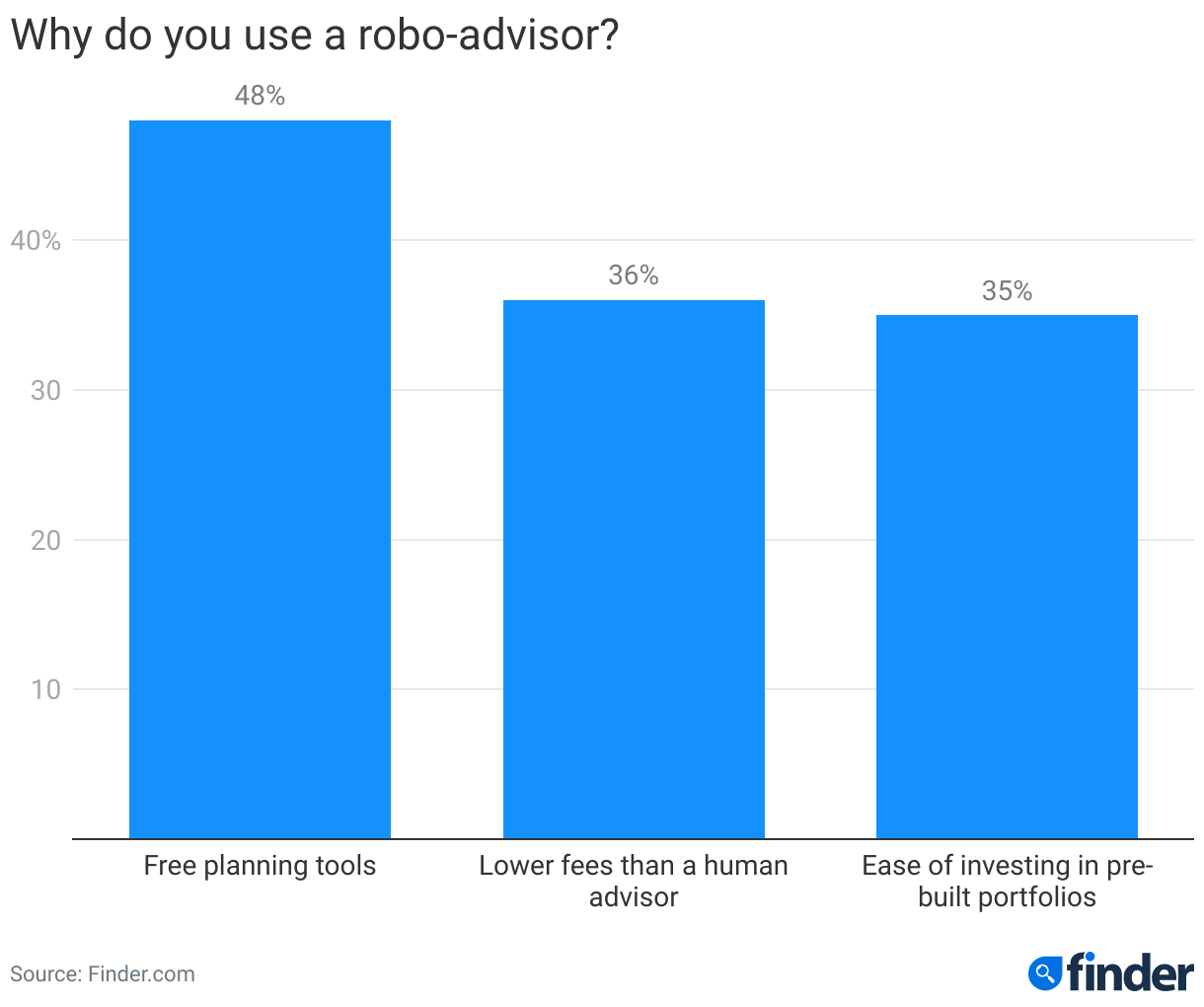

Of those that actively use Robo-Advisors within the U.S., 36% say they accomplish that as a result of they’re cheaper than a human advisor, whereas 35% say it’s the convenience of investing in pre-made portfolios, in keeping with Finder’s survey outcomes.

“With investing, less complicated is usually simpler than “tinkering,” and robo-advice makes use of the mix of know-how and the simplicity of ETFs (exchange-traded funds) together with confirmed strategies of portfolio administration.”

Six Park’s closure got here as soon as it was unclear that the adoption of robo-advice would attain ranges wanted to scale, in keeping with Garrett. The robo-advisor had tried to associate with bigger wealth and monetary recommendation companies to achieve new clientele within the lead-up to its closure, however this didn’t materialize.

“The mix of a difficult funding atmosphere and incumbents’ lack of willingness to work with fintechs (robo-advice particularly) to speed up scale stays a headwind,” mentioned Garrett.

Are Hybrid Recommendation Fashions the Future?

Regardless of the dearth of uptake, the way forward for robo-advice would possibly lie someplace in the midst of full automation and standard wealth administration.

Banking goliath JP Morgan appears to assume so — in November final 12 months, it launched its personal hybrid robo-advisor that offers buyers entry to digitally-led portfolios alongside human monetary recommendation by way of video conferencing.

Prospects get at the least one session with a human advisor who recommends a portfolio. Nonetheless, the portfolio is robotically rebalanced going ahead — except additional private recommendation is requested.

The concept is by partnering robo-advice know-how with full-service advisors — in different phrases, companies that supply human advisors — buyers can get the very best of each worlds: low-cost monetary recommendation paired with human interplay.

On the similar time, each sectors get entry to an even bigger shopper pool.

Talking at a wealth convention final 12 months, JP Morgan’s then head of product Kelli Keough mentioned the wealth sector had overestimated the demand for purely digital recommendation, as reported by the Monetary Assessment.

“I believe we forgot for a second how emotional and vital cash is to people and the way [important it is] having anyone to talk with,” mentioned Keough.

As an alternative, she believes the reply lies within the hybrid recommendation mannequin — which she says has seen an uptick within the US, at the same time as conventional robo-advice development has slowed.

JPMorgan isn’t the primary to trial the hybrid-type mannequin.

In style robo-advisor Betterment added a human recommendation element again in 2017. To entry the continuing private planning companies, you want a stability of $100,000 and are charged 0.40 % of your portfolio.

Equally, Vanguard Private Advisor prospects can go for a totally digital recommendation service, a hybrid mannequin or get a devoted private advisor. Like Betterment, charges are charged as a proportion of your funds — with the minimal stability ranging from $3,000 to $500,000 for a devoted advisor.

Whereas the non-public recommendation choices by these hybrid platforms should be out of attain for a lot of, they create a pathway that might feasibly help an investor’s lifespan.

Pure play low-cost robo-advisors could be engaging to a sure level, however as soon as a sure stage of wealth has been collected, it’s comprehensible they’ll desire a extra nuanced method that considers their private circumstances.

“Consolidation generally is a superb factor,” Garrett defined. “When a fintech has constructed a confirmed service to resolve an issue — funding assist for the mass market — and aligns with a bigger entity that may put such a service in entrance of a a lot bigger viewers in want.”

In regards to the creator:

Kylie Purcell is an Investments Analyst at Finder and a number one investments commentator. Kylie has over a decade of expertise in analyzing and presenting market updates, with experience in all areas of investments, whereas specializing in monetary merchandise, together with on-line buying and selling platforms, robo advisors, shares and ETFs, in addition to digital property and cryptocurrencies reminiscent of Bitcoin.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.

[ad_2]

Source link