[ad_1]

Listed here are some key takeaways from the month in ETF flows.

- The Morningstar Global 60/40 Index shot up 7.51% in November as shares and bonds rallied worldwide.

- Promising financial information propelled the Morningstar U.S. Core Bond Index to a 4.42% November return—its finest on report relationship again to 2000.

- The Morningstar International Markets Index, a broad gauge of worldwide equities, snapped a three-month shedding streak to the tune of a 9.21% acquire.

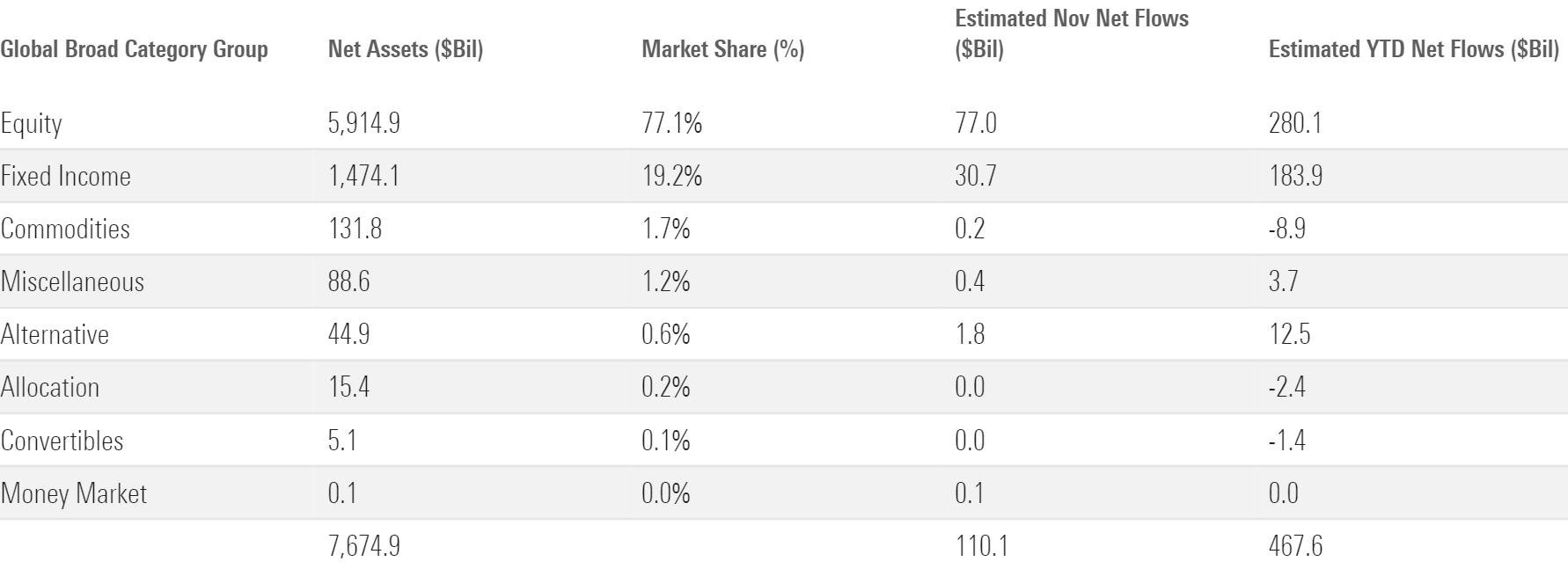

- Traders poured a whopping $110 billion into U.S. exchange-traded funds.

- Inventory ETFs reeled in $77 billion of that cash, adopted by bond ETFs with $31 billion.

- Energetic ETFs continued their dominant 2023 marketing campaign with $21 billion of inflows.

- Excessive-yield bond ETFs reversed their yr of outflows with a record-setting $11 billion haul.

- The ETF market’s “Huge Three,” iShares, Vanguard, and State Avenue, led all suppliers in November inflows.

Bonds Break By means of

Exhibit 1 exhibits November returns for a pattern of ETFs that characterize main asset lessons. A blended portfolio climbed an excellent 7% in November. Behind flourishing fairness and fixed-income returns, the Morningstar International 60/40 Index posted its finest month since November 2020.

After over a yr of dreadful efficiency, bonds lastly broke by means of in November. Vanguard Complete Bond Market ETF BND superior 4.5% in its finest month since November 2008, when buyers flocked to security within the throes of the worldwide monetary disaster. Optimistic sentiment in regards to the trajectory of interest rates primarily drove the rally. Long-term bond portfolios noticed the starkest turnaround as a result of they are typically most delicate to rates of interest. IShares 20+ Treasury Bond ETF TLT shot up 9.9% in November after sliding 13.7% over the primary 10 months of the yr. Brief-term bond methods posted milder beneficial properties—iShares Brief Treasury Bond SHV gained simply 0.5%—however they’d far much less floor to make up.

A flurry of constructive financial information powered the bond resurgence. Inflation cooled and got here in decrease than or equal to expectations, relying on the measure. That didn’t come on the expense of the economic system’s well being, as third-quarter gross domestic product data showed solid economic growth from final yr. This mix of stories satisfied the market that greater rates of interest won’t maintain for so long as feared and that the fabled “smooth touchdown” state of affairs is properly inside attain. Moreover, the Treasury Division reduce on long-term bond issuances in favor of shorter-term debt, offering one other jolt to long-term fixed-income securities.

Shares Trip the Wave

The financial components that ignited bond efficiency did the identical for equities. Vanguard Complete Inventory Market ETF VTI snapped a three-month shedding streak with a 9.4% acquire, its healthiest since November 2020. A broad vary of shares pushed the market forward, an encouraging change from early 2023 when a handful of mega-cap tech stocks shouldered the load. IShares Core S&P 500 ETF IVV and Invesco S&P 500 Equal Weight ETF RSP posted practically equivalent beneficial properties of 9.16% and 9.18%, respectively. Mid- and small-cap shares couldn’t fairly sustain with their large-cap friends, however they hewed nearer to them than earlier this yr.

Returns weren’t fairly as balanced alongside sector traces. As within the bond market, the sectors most attentive to rates of interest fared finest: Know-how Choose Sector SPDR ETF XLK led the State Avenue suite of sector methods with a 12.9% November acquire, simply forward of Actual Property Choose Sector SPDR ETF’s XLRE 12.5% return. XLK has soared 49.8% for the yr thus far by means of November—fairly the turnaround after shedding 27.7% of its worth in 2022. Power Choose Sector SPDR ETF XLE slid 0.7% in November, making it the lone SPDR sector ETF ending the month within the purple. Energy stocks have zigged whereas the broad market zagged for a lot of the previous three years. Over that span, XLE’s returns confirmed far decrease correlation to the market than any of its friends—a reminder that oil costs can drive energy-stock valuations extra acutely than the tides of the broad market.

International shares trailed the U.S. in November, however Vanguard Complete Worldwide Inventory ETF’s VXUS 8.2% acquire is nothing to sneeze at. It drew on sturdy efficiency from firms in eurozone international locations just like the Netherlands and Germany. Morningstar Indexes monitoring these markets superior 14.3% and 13.1% in November, respectively, serving to iShares MSCI Eurozone ETF EZU to an 11.1% November return. Korean and Taiwanese equities posted glorious beneficial properties final month, too, although milder China-stock returns weighed on most Asia-Pacific and emerging-markets portfolios.

ETF Flows Take Off in November

Traders piled a whopping $110 billion of latest cash into ETFs final month. Scaling for measurement, that interprets right into a 1.57% natural development fee—their finest since March 2021. After a yr of touch-and-go flows, ETFs are abruptly poised to blow previous the $500 billion annual influx threshold that regarded properly out of attain only a month in the past. They’ve raked in $477 billion to this point this yr.

Inventory ETF Flows Shine

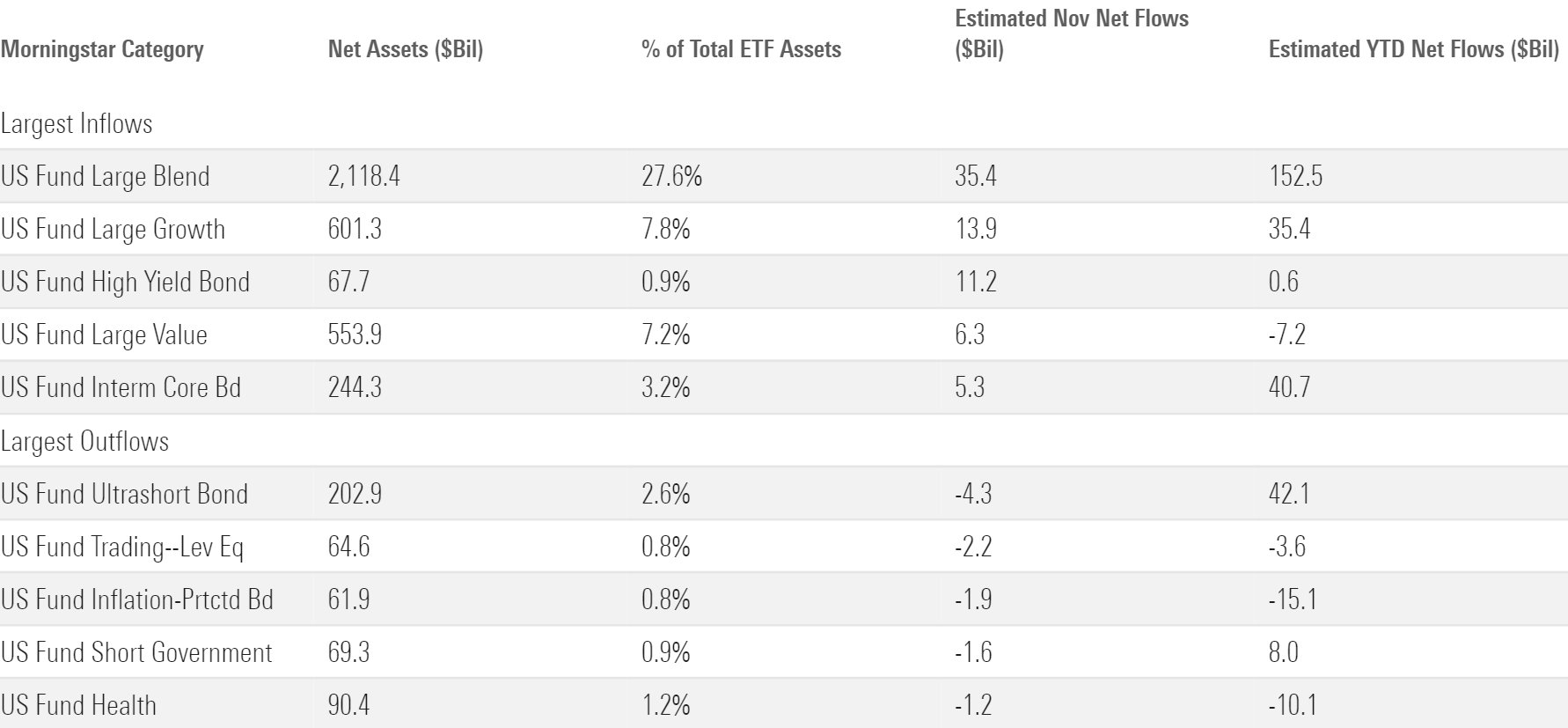

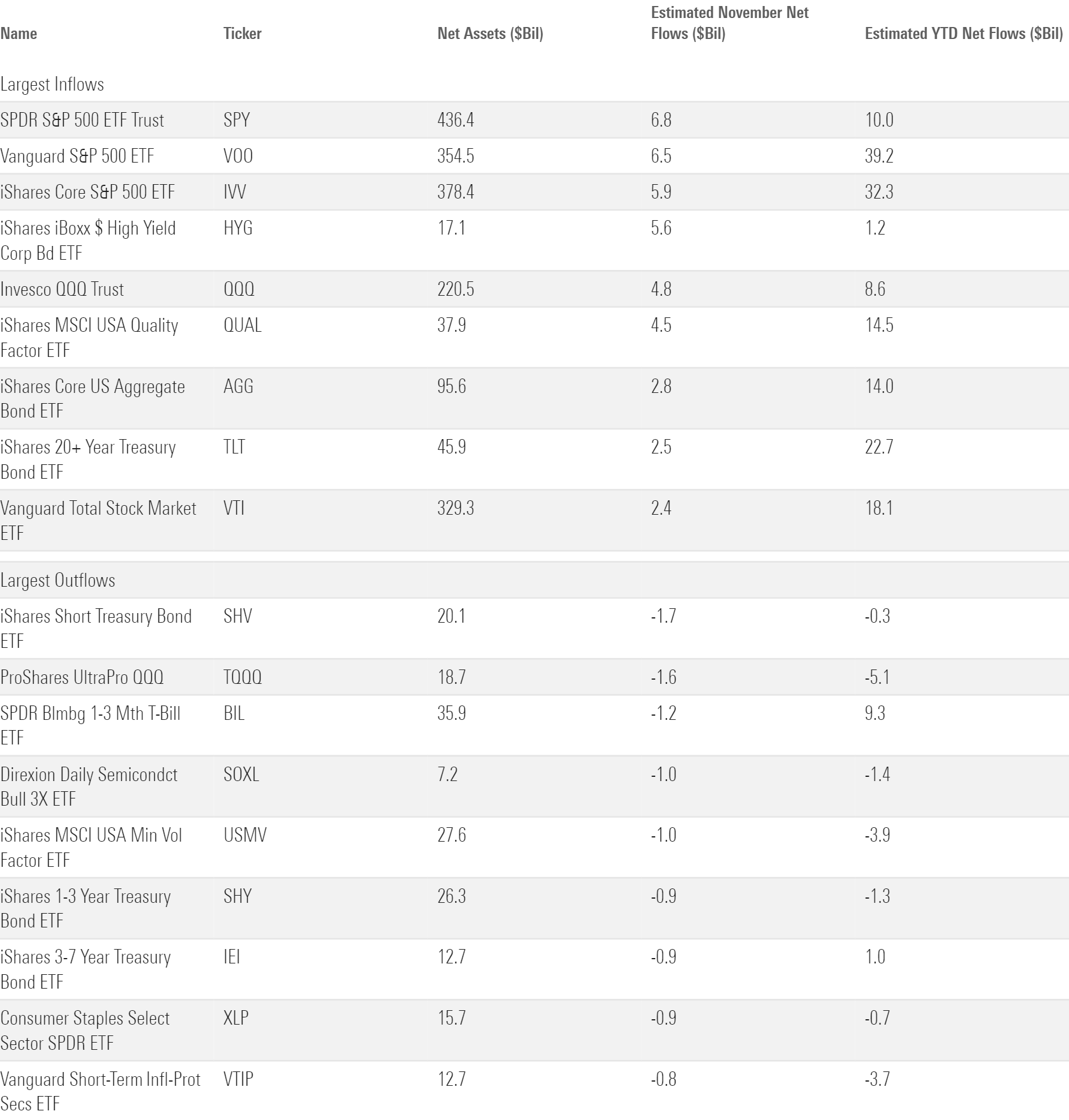

A powerful month within the markets was all buyers wanted to reload on inventory ETFs. U.S. fairness funds led the cost, the place all 9 Morningstar Classes in that cohort completed November with inflows. Predictably, large-blend funds set the tempo, with $35 billion of latest cash. However inflows into the large-growth class have been much more noteworthy. Led by the irrepressible Invesco QQQ Belief QQQ, the class hauled in $14 billion—its second-largest month-to-month consumption ever. Large-value funds have navigated a difficult year, however even they joined the motion with a $6 billion haul, their finest month since final December.

Traders weren’t as enthused about funds that concentrate on overseas shares. The international-equity section pulled in $6 billion—a good sum, however a far cry from their home counterparts, even when scaled for belongings. China-region funds had a standout month, nevertheless. Their $476 million November haul doesn’t bounce off the web page, but it surely marked the class’s first month of inflows since January. The Morningstar China Index has pulled again 8.7% over the primary 11 months of 2023—about 18 proportion factors behind the Morningstar Global Markets Index.

Sector-equity funds righted the ship with $5 billion of November inflows after bleeding a complete $16 billion over the three months prior. In step with the month’s bullish theme, buyers favored cyclical sectors to defensive ones. Know-how funds reeled in $5 billion to hold the day, whereas healthcare and client defensive methods shed about $1 billion apiece. That every one mentioned, until the sector-equity group can construct on this month with greater than $4 billion of December inflows, 2023 will mark its worst month of outflows on report (breaking the report set final yr).

Bond ETF Flows Quietly Pile Up

Bond ETFs performed second fiddle to shares by way of absolute inflows final month, however their 2.2% natural development fee handily outpaced their fairness counterparts. Thus far in 2023, bond ETFs’ $184 billion haul translated right into a stellar 14.3% natural development fee, properly forward of inventory ETFs’ 5.6% clip.*

Low-risk, conservative bond portfolios have supercharged the broader fixed-income cohort for a lot of 2023, however in November, it was the riskier classes that took the reins. Getting into November, high-yield bond funds had shed $10.4 billion on the yr. They pulled in $11.2 billion in November—their finest month of absolute flows on report. Company bond funds collected extra final month ($4.5 billion) than they did over the ten months prior ($2.2 billion).

In the meantime, uber-safe ultrashort bond funds bled $4.3 billion in November, essentially the most amongst all Morningstar Classes. It led all fixed-income classes with practically $47 billion in year-to-date flows coming into the month. Authorities-bond ETFs collected $3 billion in November—a fantastic sum, however not a lot in contrast with the remainder of the group and a far cry from the ransoms they pulled in earlier this yr. Clearly, the risk-on sentiment that drove buyers into inventory ETFs performed a job in shaping fixed-income flows as properly.

Fast Hits From Across the Market

- Sustainable funds barely joined in on the enjoyable. After pulling in a modest $1.2 billion on the month, the cohort has shed $5.6 billion for the yr thus far by means of November.

- Ditto for thematic funds. They bled over $500 million as outflows from power transition funds like iShares International Clear Power ETF ICLN battled outflows. Maybe buyers are rising weary of timing their thematic fund purchases poorly.

- Energetic ETFs continued their dominant 2023 campaign in November. Traders dumped about $21 billion into them, pushing their year-to-date inflows to over $116 billion. That helped construct energetic ETFs’ cushion on their record-setting yr, as they collected $90 billion in 2022.

- Momentum for nontraditional-stock and, extra particularly, covered-call ETFs appears to be dissipating. The spinoff revenue class, which homes all covered-call funds, collected about $1.1 billion in November—nonetheless an honest sum, however less than snuff with the month-to-month $2 billion-plus inflows they routinely collected in late 2022 and early 2023. JPMorgan Fairness Premium Earnings ETF JEPI posted its mildest month of inflows since January 2021, when it was simply eight months previous.

- However, momentum appears to be constructing for options ETFs. They absorbed about $1.8 billion in November, their finest month since October 2021. That’s 5 consecutive months of inflows north of $1.5 billion for the cohort that has seized the rise of buffer ETFs, which use choices to make sure buyers have a ground or cap on their fund efficiency. Learn extra in regards to the nuances of buffer ETFs here.

- Some contrarians light the overwhelming bullish sentiment final month. Inverse-equity funds collected $1.8 billion, whereas their leveraged-long counterparts bled practically $2.2 billion. For his or her sake, let’s hope buyers who “bought the rip” didn’t transfer too early within the month.

Fund Households

The “Huge Three″ ETF suppliers affirmed their place atop the market in November. Their rating for November inflows matched their rating by complete belongings: iShares led the best way with $32 billion, adopted by Vanguard with $23 billion and State Avenue with $18 billion.

IShares loved its most profitable month since final Could as a result of its fairness choices lastly returned to favor. These funds collected $17 billion on the month after toiling in outflows all yr, a welcome breakthrough for the indexing large. Vanguard has had no such troubles. Prefer it has all yr, it leaned on inventory and bond inflows at practically a three-to-one fee—a recipe that has propelled it properly forward of the ETF-provider pack in 2023 flows. State Avenue’s strong month owes partly to its suite of sector ETFs. Whereas the $1.9 billion they absorbed doesn’t bounce off the web page, it’s an enchancment from the three consecutive months that preceded November, over which these funds bled greater than $7 billion in complete.

Constancy is not any beginner to the world of ETFs, however November was its coming-out get together. It entered the month with roughly $36 billion in ETF belongings and completed with practically $49 billion. That’s the product of each glorious market returns and a slew of mutual fund-to-ETF conversions—nearly $9 billion price of them, to be precise. Constancy is the second-largest mutual fund supplier in the US. It might climb shortly up the ranks of the biggest ETF suppliers ought to it transfer extra of its behemoth mutual funds into the ETF automobile.

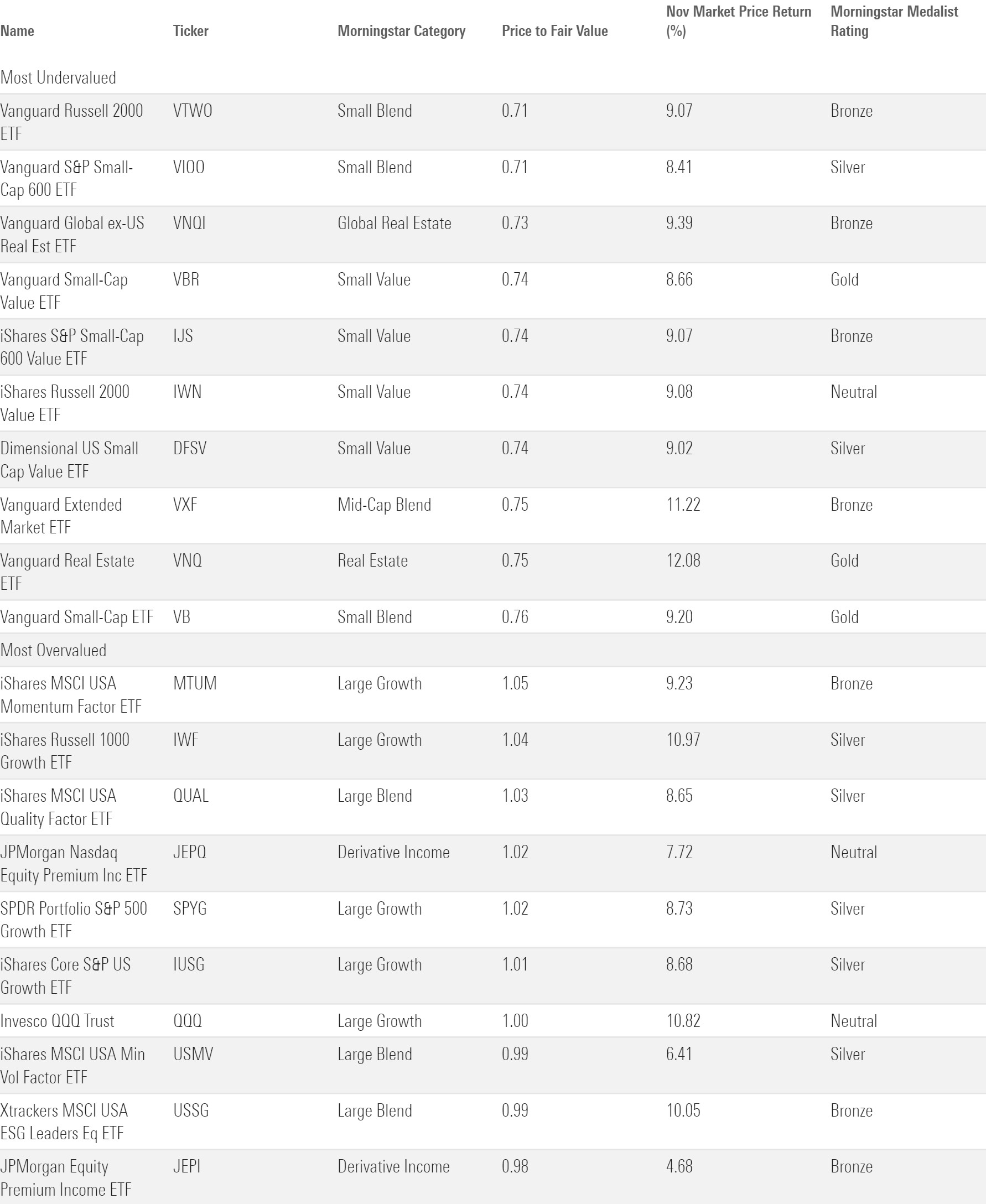

Actual Property ETFs Look Undervalued Regardless of Stellar November

The fair value estimate for ETFs rolls up our fairness analysts’ honest worth estimates for particular person shares and our quantitative honest worth estimates for shares not coated by Morningstar analysts into an mixture honest worth estimate for inventory ETF portfolios. Dividing an ETF’s market worth by this worth yields its worth/honest worth ratio. This ratio can level to potential bargains and areas of the market the place valuations are stretched.

The widespread November rally pumped up worth/honest worth ratios all around the board. IShares MSCI ACWI ETF ACWI, which touches a lot of the worldwide inventory market, noticed its ratio climb from 0.81 to 0.93 after it gained 8.9% in November. That sub-one ratio signifies that international shares may still be undervalued, nevertheless, and sure pockets of the market nonetheless sport reductions match for Black Friday.

U.S. small-value funds head up that listing. The six analyst-rated small-value funds traded 25% under their honest worth as of November 2023—most amongst all broad-based Morningstar Classes. Subpar efficiency explains many of the low cost: iShares S&P Small-Cap 600 Worth ETF IJS scratched out a 1.2% acquire for the yr thus far by means of November—about 19.5 proportion factors behind IVV. Small-value funds have tested investors’ patience, however they have been neck-and-neck with their bigger friends final month and have loads of room to run shifting ahead.

For extra concentrated buyers, no sector regarded as low-cost as actual property when November concluded. Vanguard Actual Property ETF VNQ traded at a paltry 0.75 worth/honest worth ratio—after it notched a 12.1% return in November. The REITs this technique favors are typically fairly delicate to interest-rate fluctuations. The fund might proceed to climb ought to the market proceed to cost in a lower-rate regime.

*This OGR calculation excludes buying and selling devices within the Miscellaneous U.S. Class Group.

[ad_2]

Source link