[ad_1]

2024 Inventory Market Outlook Key Takeaways

- The U.S. inventory market is now buying and selling equal to a composite of our honest worth estimates.

- Worth shares and small-cap shares nonetheless commerce at enticing reductions.

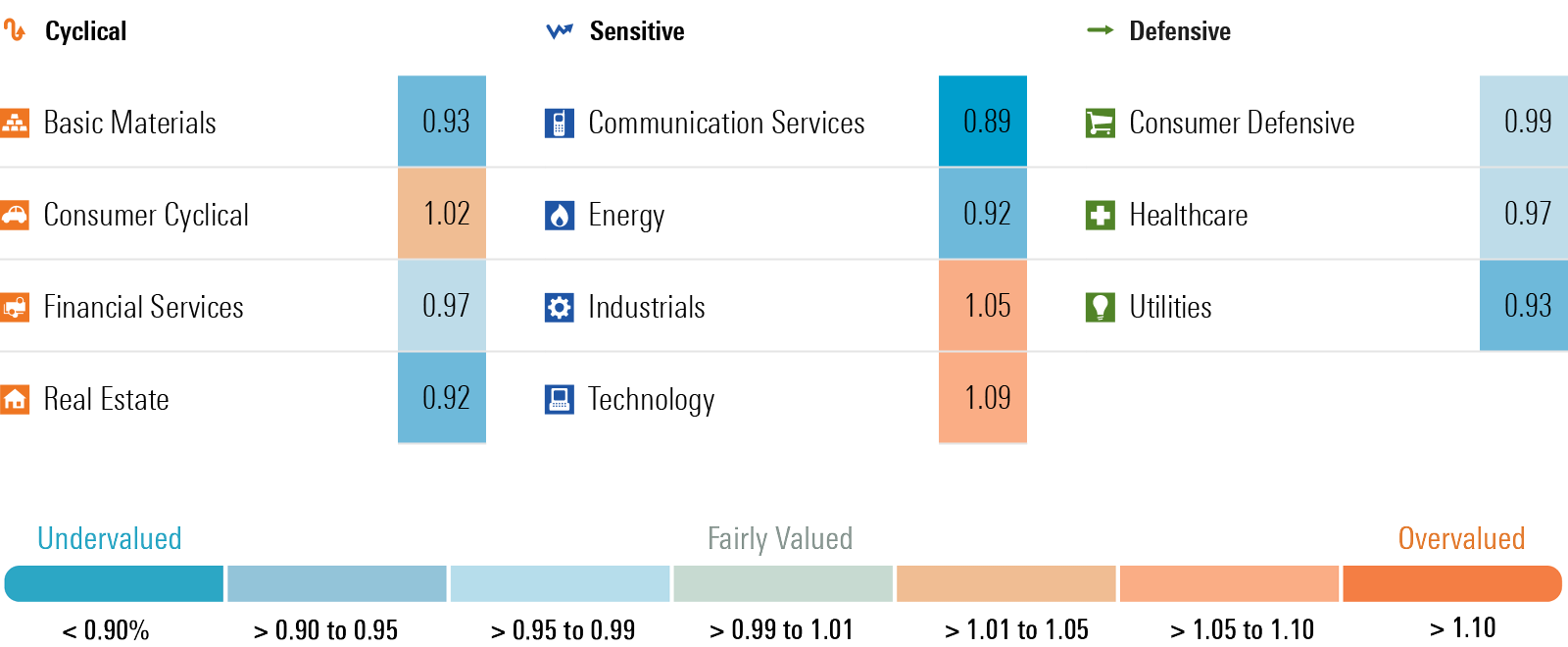

- The know-how sector moved again to a selection for underweighting together with industrials, whereas communications, fundamental supplies, actual property, and utilities are enticing overweightings.

- The speed of financial progress is forecast to gradual in 2024, however no recession.

As long-term rates of interest rose and the 10-year U.S. Treasury bond neared 5% final fall, shares bought off, dropping properly into undervalued territory. Nevertheless, this 12 months’s “Santa Claus Rally” got here early as long-term rates of interest subsided in November after which the rally was boosted even additional following the December Fed assembly. The market interpreted Federal Reserve Chair Jerome Powell’s remarks to point that not solely is the Fed achieved mountaineering charges, however additionally it is now contemplating when to start easing financial coverage.

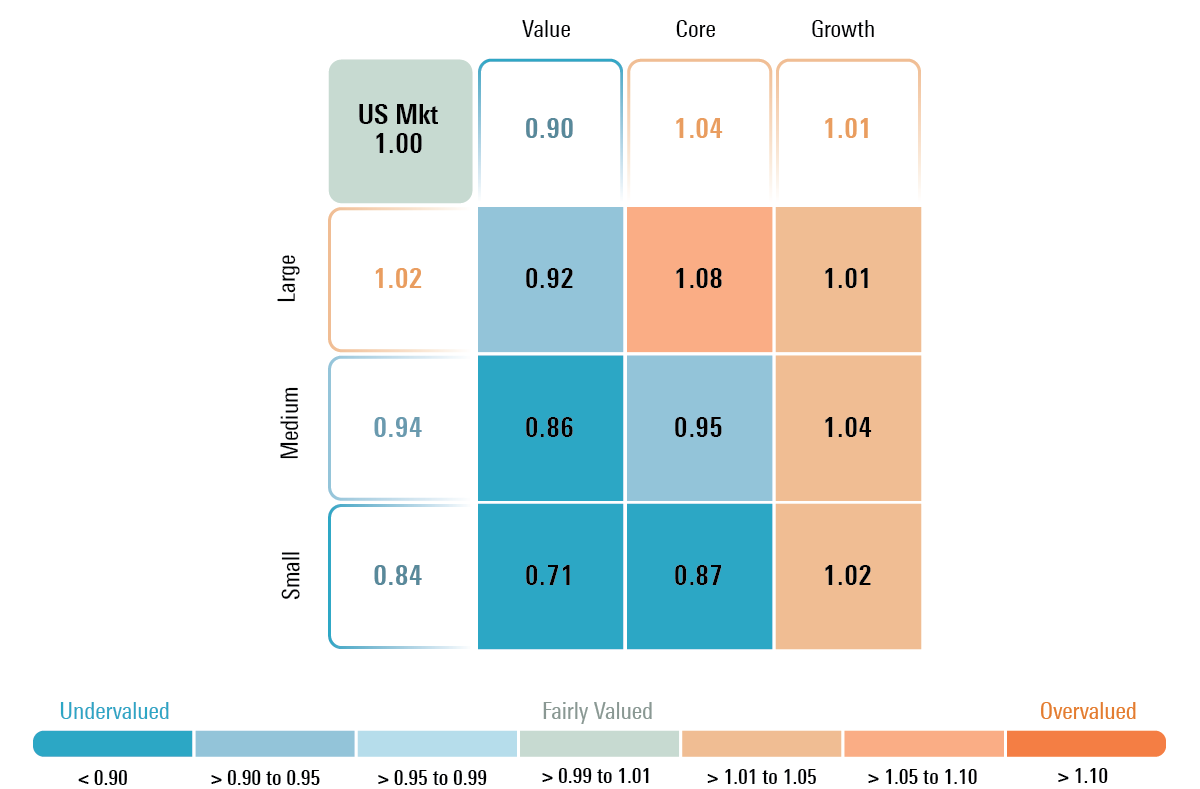

In line with a composite of the over 700 shares we cowl that commerce on U.S. exchanges, as of Dec. 21, 2023, the U.S. fairness market was buying and selling at a value/honest worth of 1.00, which means that the market is the same as a composite of our honest worth estimates.

With Shares Pretty Valued, How Ought to Traders Place Themselves in 2024?

After 4 years, 2024 is lining as much as be the 12 months that the financial system and particular person habits have lastly recovered and normalized. The large disruptions attributable to the pandemic and dislocations attributable to these disruptions are behind us. Whereas we forecast that the speed of financial progress will gradual and shares have already rallied and are nearing their highs, we nonetheless see a number of undervalued areas that present comparatively massive margins of security.

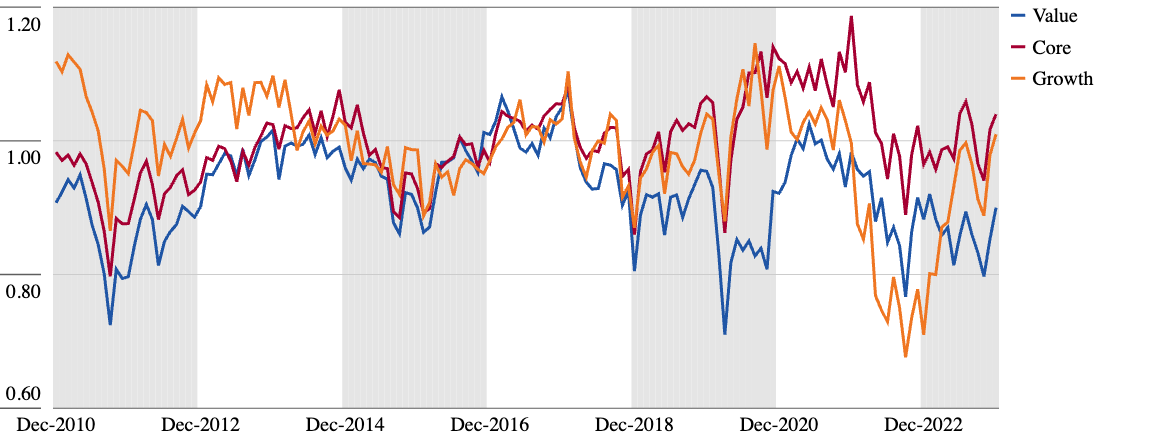

By capitalization, small-cap shares stay probably the most enticing at a 16% low cost, adopted by mid-caps at a 6% low cost, whereas massive caps are just a little above honest worth. By class, for long-term traders, based on our valuations, worth shares stay probably the most enticing, buying and selling at a ten% low cost to honest worth, whereas core shares are buying and selling into overvalued territory and progress are basically at honest worth.

After dominating the market within the first half of 2023, the “Magnificent Seven” (Apple AAPL, Amazon.com AMZN, Alphabet GOOGL, Meta Platforms META, Microsoft MSFT, Nvidia NVDA, and Tesla TSLA) have run out of steam. Solely Alphabet stays undervalued, whereas 5 others are actually buying and selling in honest worth territory and Apple is overvalued.

Wanting ahead, we anticipate additional positive aspects will proceed to be pushed by a widening out of returns throughout the market. In reality, we’ve already began to see this development emerge. Features are more and more spreading out throughout different areas available in the market that had been left behind. For instance, the Magnificent Seven accounted for 75% of the market return on the finish of June, however as of Dec. 21, they account for under 52%. Particularly, we proceed to see the most effective alternative for traders within the worth class, which stays probably the most undervalued based on our valuations, in addition to down in capitalization into small-cap shares.

Over the subsequent few months, we predict the subsequent check for the markets will are available February and March when firms report earnings. We aren’t as involved about earnings as we’re that administration groups could look to decrease the bar available on the market’s expectations for earnings progress in 2024 as the speed of financial progress is poised to gradual.

Historic Comparability of Morningstar’s Valuations by Capitalization and Class

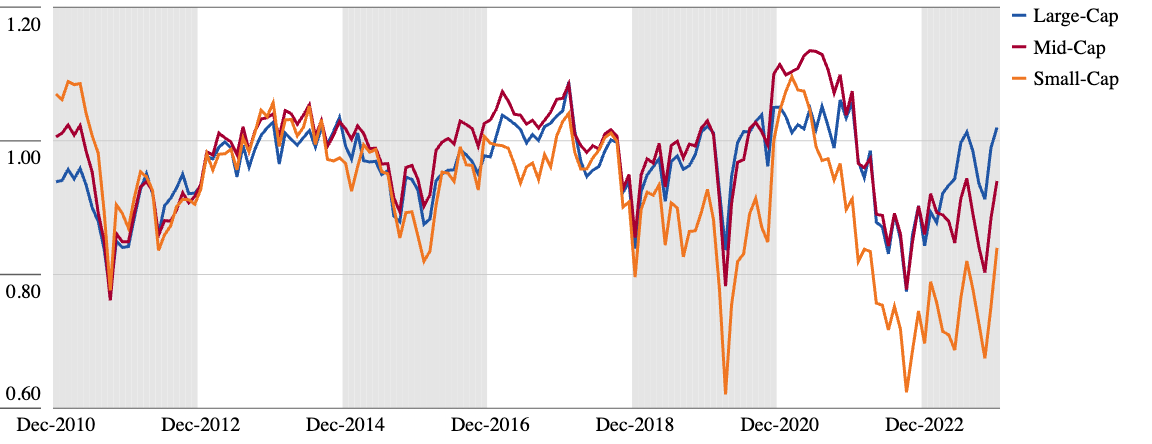

On a value/honest worth foundation, small-cap shares stay close to a few of the best reductions to large-cap and mid-cap shares that we’ve seen since 2010. Small-cap shares bought off more durable and sooner through the early levels of the pandemic as traders feared smaller firms wouldn’t have the wherewithal to outlive. This previous fall, small-cap shares have been beneath extra strain as traders have been involved that small-cap shares can be extra adversely affected by rising rates of interest as they usually have shorter length debt and will have to refinance at excessive rates of interest. As well as, financial institution funding has turn out to be extra restrictive as banks are much less prepared to increase loans to greater danger credit.

In our view, this units the stage for small-cap shares to outperform. We expect 2024 would be the first 12 months that each the disruptions from the pandemic and all the next dislocations attributable to these disruptions shall be behind us. Whereas the speed of financial progress could gradual, we anticipate that, in a extra normalized financial atmosphere, the prior fears about small-cap solvency ought to alleviate. As well as, we forecast rates of interest throughout the curve will subside in 2024 and 2025, thus mitigating a lot of the refinancing danger.

Worth shares additionally look like properly positioned to outperform. Many progress shares have been in a position to initially profit from the pandemic. For instance, as staff shifted to working from residence, they required a big selection of technological providers and merchandise. Worth shares have been hit by a double whammy of near-term earnings deterioration as they disproportionately suffered from a fast change in shopper habits and subsequent financial dislocations, in addition to traders making use of decrease market valuation multiples.

Notable Adjustments in Sector Valuations and Outlooks

No sector has been as unstable because the know-how sector in 2023. Expertise began 2023 because the third-most undervalued sector as in contrast with our valuations. Expertise rallied as much as honest worth, overshot to the upside, retreated again to honest worth, and has bounced again properly into overvalued territory. Shopper cyclicals began 2023 because the second-most undervalued sector, but it’s now absolutely valued following its outperformance. Lastly, industrials have moved into overvalued territory.

Whereas actual property stays considerably undervalued, following its sturdy fourth-quarter efficiency, the title for many undervalued sector returns to communications. Communications began 2023 as probably the most undervalued sector, and even after incorporating its above-market returns, it stays undervalued. And it’s not simply Alphabet that’s undervalued—we see undervaluation throughout a large swath of conventional communications shares.

After beginning the 12 months as probably the most overvalued sector, power is now one of many extra undervalued sectors, following its underperformance for the 12 months thus far as oil costs have fallen. After dropping precipitously as rates of interest rose, the utility sector is now undervalued. We proceed to seek out worth within the fundamental supplies sector because the bubble in lithium costs has popped and fallen too far to the draw back and gold-mining firms present a horny upside choice.

Our Outlook for the U.S. Economic system and Financial Coverage

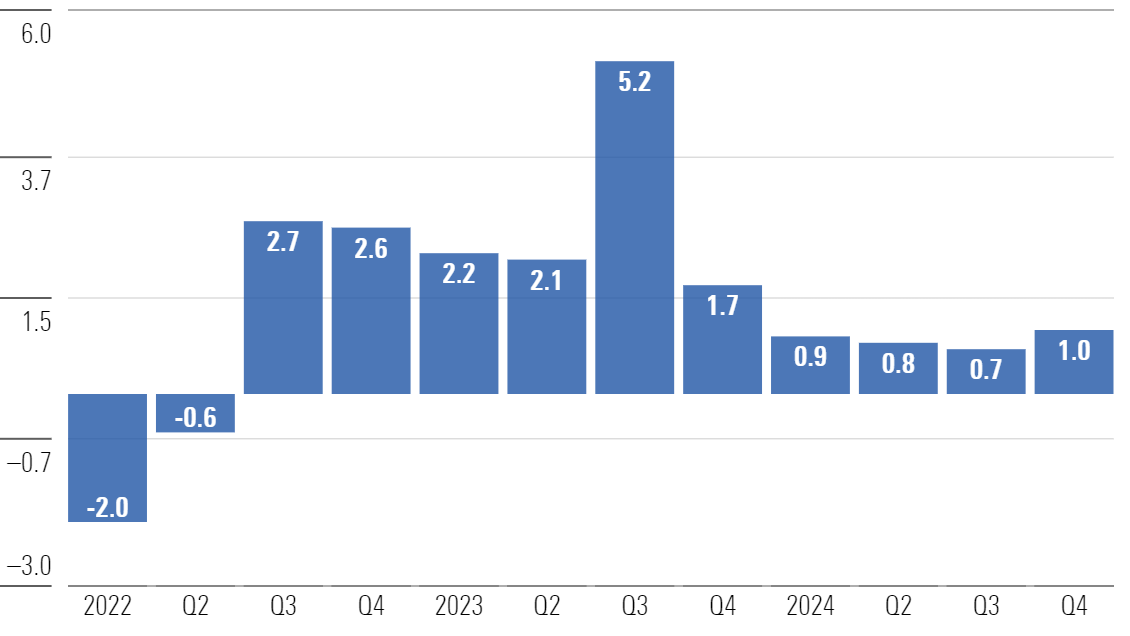

The U.S. financial system continued to defy restrictive financial coverage in 2023 as actual gross home product surged to five.2% within the third quarter, main us to extend our actual GDP forecast for 2023. Nevertheless, we nonetheless anticipate that greater rates of interest, restrictive financial coverage, and tight lending restrictions will take their toll on the financial system. We forecast that the speed of financial progress has begun slowing within the fourth quarter of 2023 and the speed of progress will proceed to gradual till bottoming out within the third quarter of 2024. From there, our expectation for simpler financial coverage will permit financial progress to start to broaden steadily thereafter.

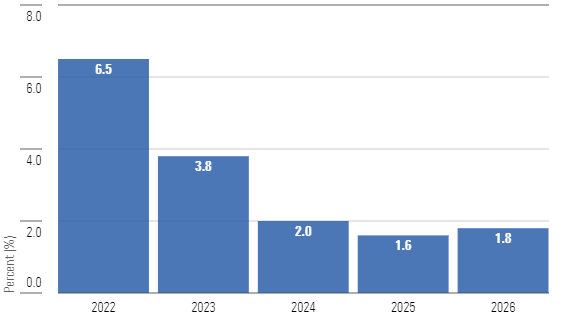

Each headline and core Shopper Value Index readings have remained on a downward development in 2023. We proceed to forecast that inflation will reasonable over the course of 2024 and into 2025. In line with our projections, the foremost drivers of excessive inflation, akin to provide chain bottlenecks, shortages, and different disruptions, will additional unwind over the subsequent few years, offering extended deflationary strain. In reality, our below-consensus forecast requires inflation to fall under the Fed’s 2% inflation goal in 2025 earlier than starting to barely rise again up.

As we anticipated, the Federal Reserve held the federal-funds price regular at its December assembly. We had beforehand famous that we had anticipated the July hike can be the ultimate interest-rate improve of this financial coverage tightening cycle.

This financial tightening cycle has been the steepest and quickest over the previous 40 years, but far much less restrictive than the coverage through the Seventies and ‘80s. Whereas the financial system has held up higher than anticipated within the face of this tightening cycle, we nonetheless anticipate that the speed of financial progress will gradual all through most of 2024.

Wanting ahead, we anticipate that the mixture of slowing financial progress and declining inflation will immediate the Fed to start loosening financial coverage and start decreasing the federal-funds price, probably as early as March 2024. We forecast six interest-rate cuts over the course of 2024, double that of the Fed’s present projection.

2024 Market Outlook Webinar

Be a part of me and Morningstar’s Chief U.S. Economist Preston Caldwell on Wednesday, Jan. 10, 2024, at 11 a.m. Central/midday Jap as we:

- Break down our valuations and establish undervalued alternatives throughout classes, sectors, and shares.

- Spotlight investable long-term secular progress themes.

- Present our forecasts for actual U.S. gross home product, inflation, and rates of interest.

- Reply dwell viewers questions.

Register here.

[ad_2]

Source link